Return to Press Room

Buy Now, Pay Later Stretches Limits of Consumer Credit, According to Achieve Center for Consumer Insights Study

The share of consumers with recent BNPL accounts who need help to address unsustainable debt has grown over 50% since 2021, according to the first study by the Achieve Center for Consumer Insights

September 22, 2022

SAN MATEO, Calif., Sept. 22, 2022 — The rapid growth of buy now, pay later (BNPL) financing has had a cascading effect on consumer debt levels, according to a new study by Achieve, the leader in digital personal finance.

The study found that a growing number of already debt-stressed individuals are leveraging BNPL financing to stretch their available credit limits before ultimately needing assistance to address unsustainable debt levels.

Achieve Center for Consumer Insights

The study is the first in a planned series by the new Achieve Center for Consumer Insights, an ongoing initiative that leverages Achieve’s team of digital personal finance experts to provide a view into the state of Achieve’s members, with a particular emphasis on data and emerging trends in personal loans, consumer debt and home equity loans.

In addition to sharing insights gleaned from Achieve’s proprietary data and analytics, the Achieve Center for Consumer Insights intends to publish in-depth research, bespoke data and thoughtful commentary in support of Achieve’s mission of helping everyday people get on, and stay on, the path to a better financial future.

“Introducing the Achieve Center for Consumer Insights alongside the debut of the new Achieve brand and our expanded suite of digital personal finance offerings reflects our commitment to supporting every step of our members’ financial journeys. We look forward to helping educate consumers on the state of their finances and keeping them updated on economic developments that affect household balance sheets,” said Achieve Co-Founder and Co-CEO Brad Stroh. “In addition, we hope that the data and research produced by the Achieve Center for Consumer Insights will encourage thoughtful dialogue among technology and financial services professionals; academic and advocacy groups; policymakers and other stakeholders.”

BNPL’s Effect on Consumer Debt

As of June 2022, the percentage of Achieve debt relief members with BNPL accounts on their credit reports has grown 58% compared to January 2021. While the segment of Achieve debt relief members with BNPL tradelines is still relatively low, it is also likely an underrepresentation of the BNPL industry’s entire reach because very few BNPL transactions are currently reported to the three major credit bureaus.

Many BNPL users are apt to use this financing to stretch out their credit limits on existing credit cards and other accounts, according to Achieve data — even though BNPL is frequently touted as a product designed for consumers who want to avoid credit cards and other traditional forms of credit.

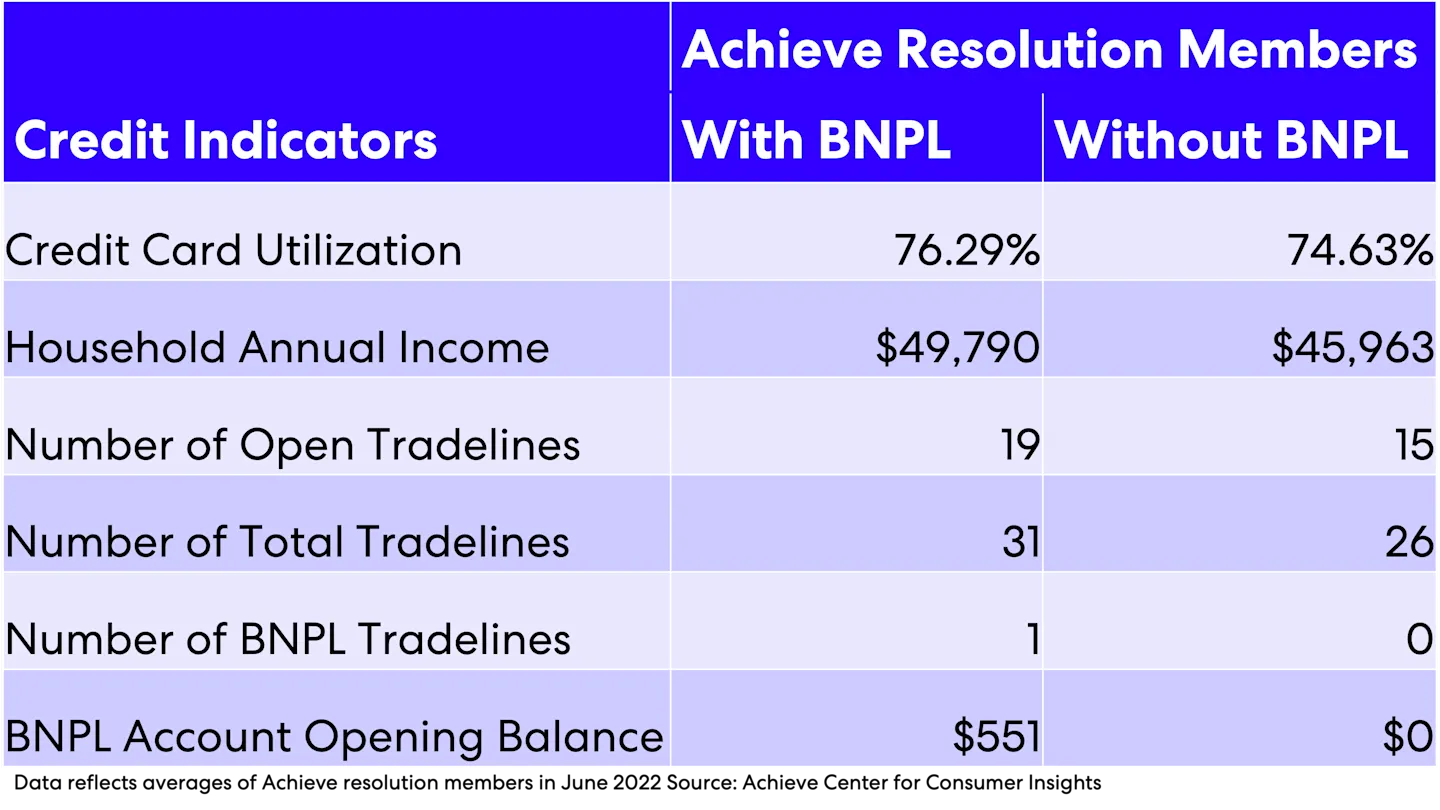

Achieve debt relief members with BNPL loans on their credit reports have more open tradelines on their credit file than members without BNPL loans. They also have more total tradelines — which includes both current tradelines and former accounts that were closed less than 10 years ago — reported on their credit files. Achieve members with BNPL accounts had slightly higher credit card utilization rates than Achieve debt relief members without. They also had lower average credit scores than members without BNPL accounts. However, BNPL users had slightly higher household incomes (see Figure 1).

Figure 1: Credit Profile of Achieve Debt Relief Members

“The ongoing expansion of the BNPL’s industry’s reach comes alongside a period of historic inflation and rising interest rates that’s putting a strain on household finances,” said Achieve Co-Founder and Co-CEO Andrew Housser. “Buy now, pay later can be attractive for consumers seeking an interest-free option to pay for purchases over time. But even without finance charges consumers can still get over-extended using these loans.”

The average balance on the BNPL accounts of Achieve debt relief members has decreased since the beginning of 2021, reflecting the widespread availability of BNPL as a digital payment option in both virtual and physical point-of-sale. In June 2022, nearly 50% of Achieve debt relief members with at least one BNPL account were Millennials and about one-third were Gen Xers. Achieve’s findings echo a recently released Consumer Financial Protection Bureau study, which highlights the growth in BNPL loan volume and consumer late fees.

Additional Key Findings from Achieve Debt Relief

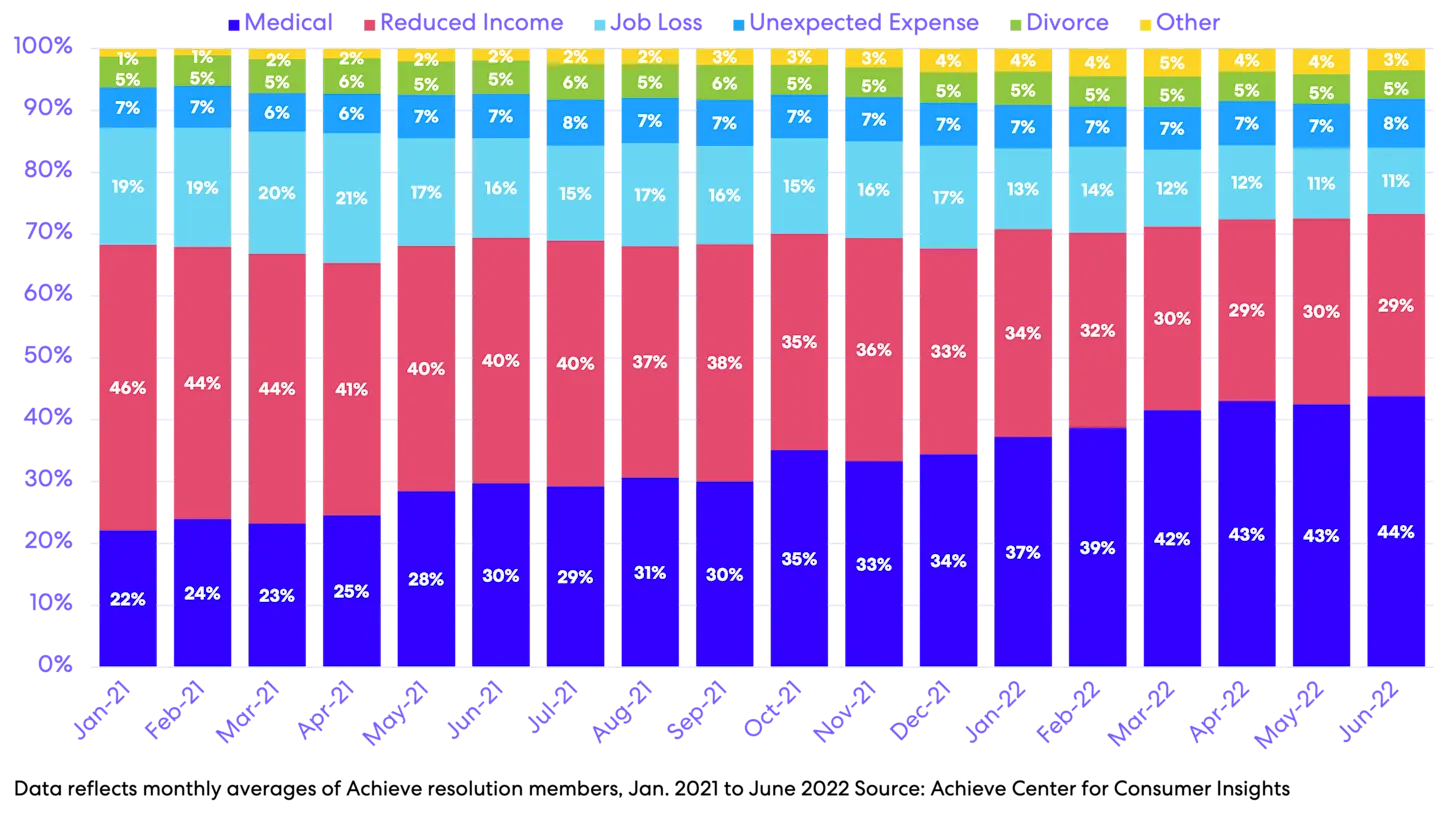

Evolving Financial Hardships: Medical expenses have become the leading reason why consumers sought Achieve’s help with debt, reflecting an ongoing trend that began in early 2021 (see Figure 2). Reduced income and job loss continue to account for a large portion of member hardships, but have declined over this same period of time.

Figure 2: Achieve Debt Relief Member Hardships

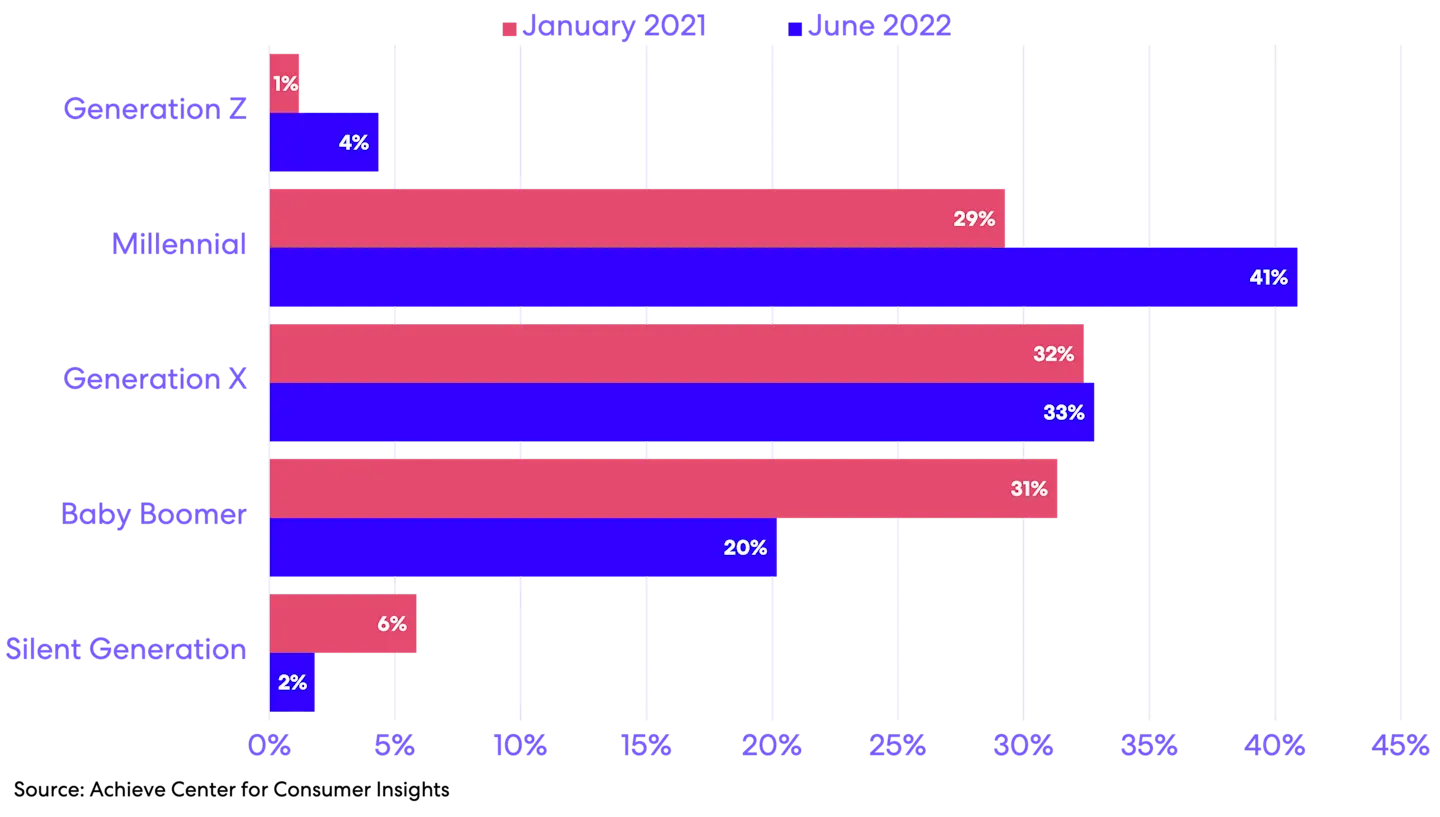

Generational Shifts: Millennial and Gen Z members seeking help with debt through Achieve debt relief has grown since January 2021, while the share of Silent Generation and Baby Boomer members is declining (see Figure 3).

Figure 3: Achieve Debt Relief Members, by Generation

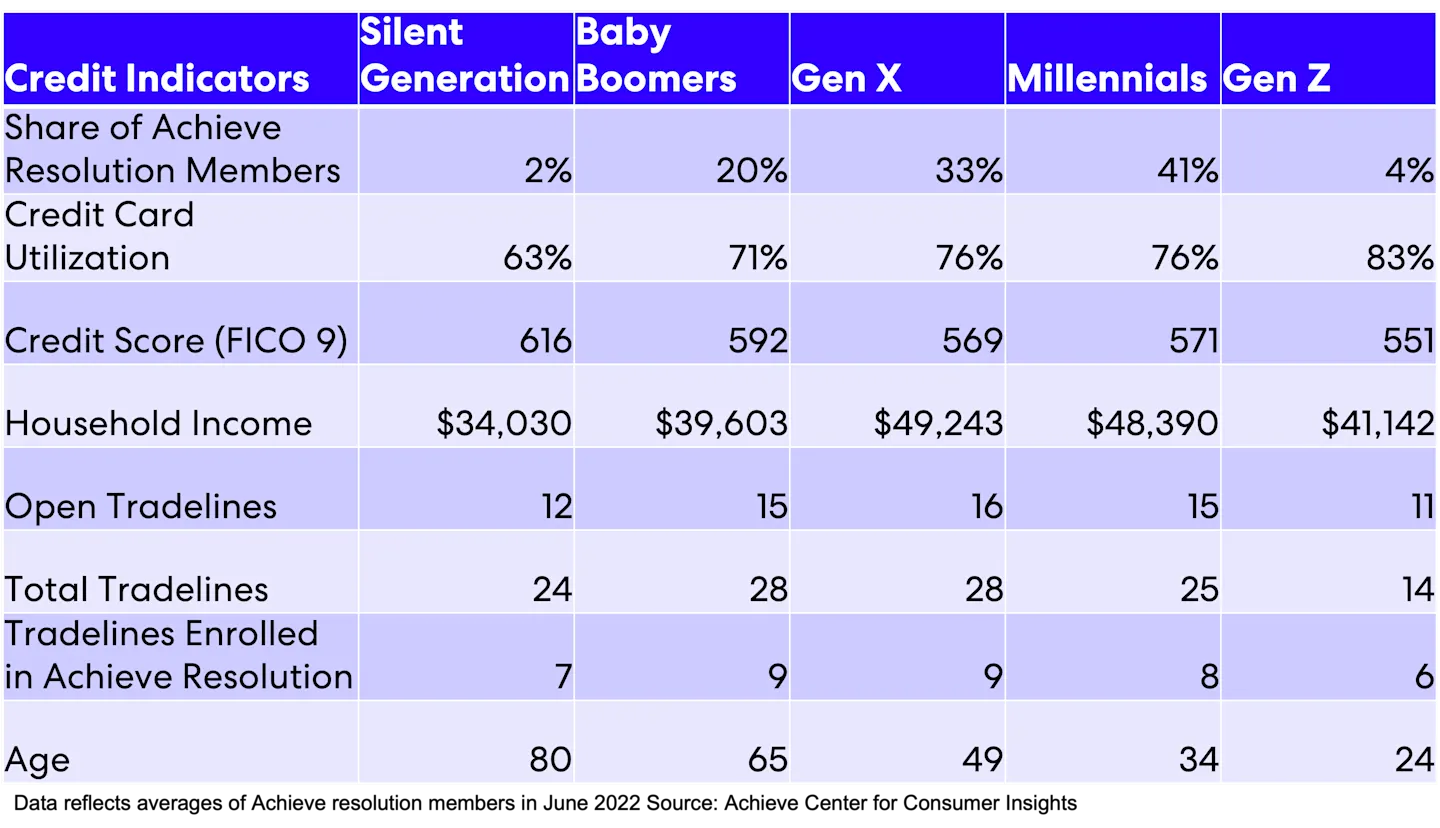

Strong parallels exist between Gen X and Millennials across many key credit indicators, even though the average age of Gen Xers enrolled in Achieve debt relief is 15 years older than that of Millennials (see Figure 4). The two generations have comparable credit scores, household incomes, and credit histories, however, Gen Xers average more credit report tradelines. In addition, the three youngest generations all have higher average household incomes than Achieve debt relief members from the Silent and Baby Boomer generations.

Figure 4: Achieve Debt Relief Key Credit Indicators, by Generation

Key Findings from Achieve Personal Loans

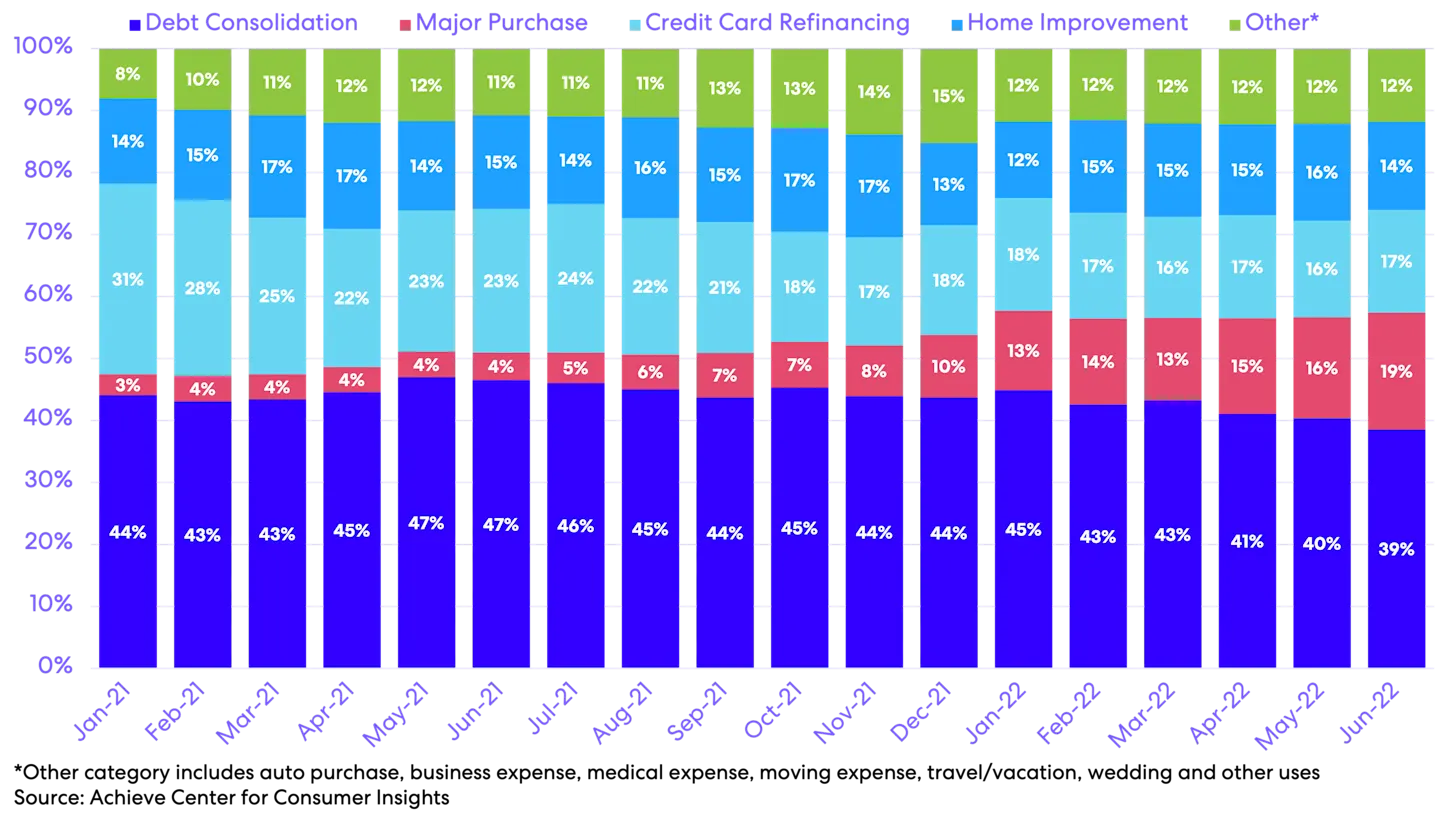

Dealing with Debt: Debt consolidation and credit card refinancing are the leading reasons why Achieve members obtain personal loans, consistently accounting for over half of all new loan originations since the start of 2021 (see Figure 5). However, the portion of members using personal loans to pay for major purchases is on the rise, accounting for 19% of the loans obtained in June 2022.

Figure 5: Member Uses of Achieve Personal Loan Funds

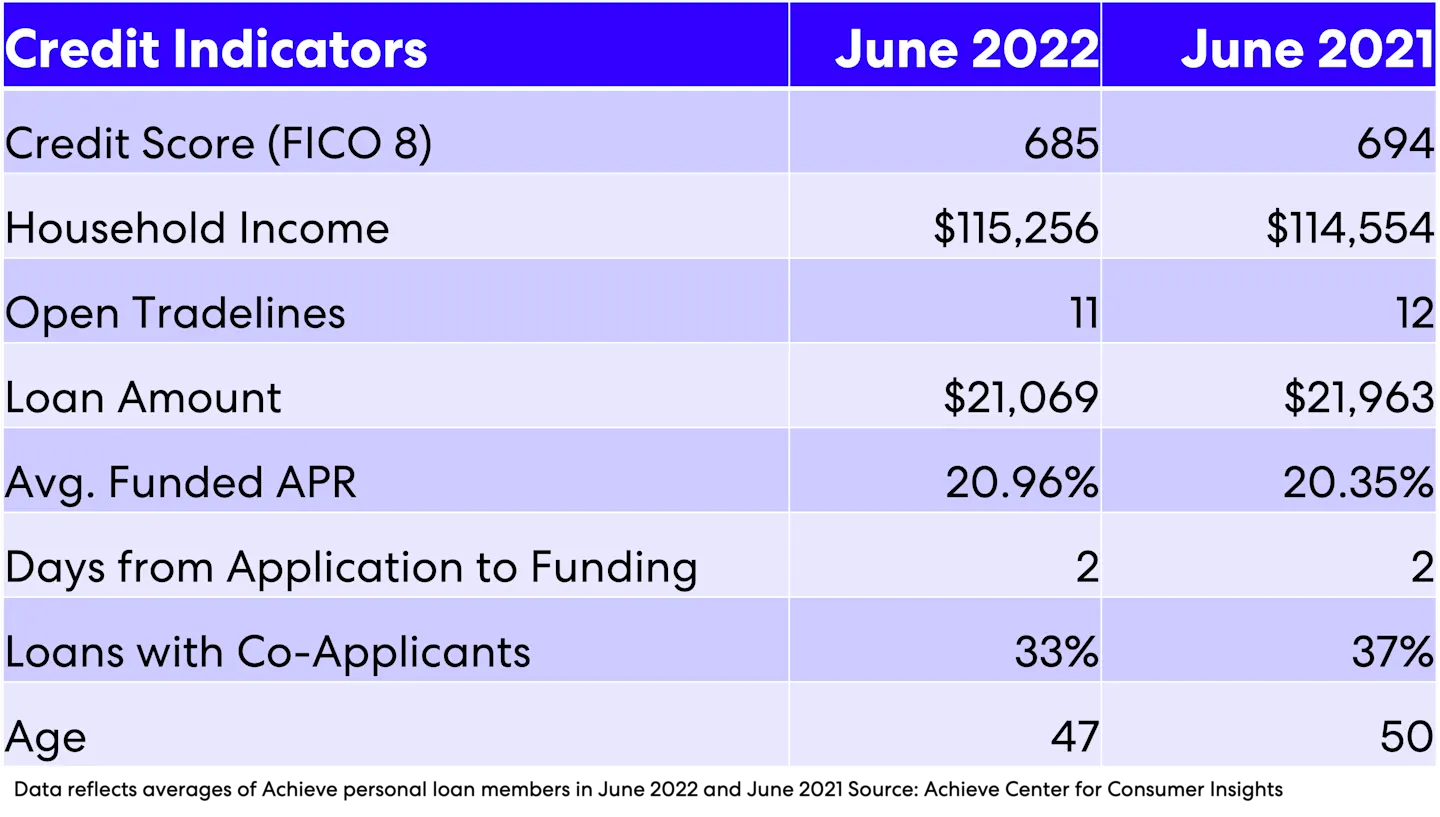

Personal Loan Profile: Achieve personal loan members had an average of 11 open tradelines when applying for a personal loan in June 2022. Loan amounts range from less than $10,000 to over $35,000, with an average starting loan balance of just over $20,000. Key credit indicators for Achieve personal loan members remain largely unchanged compared to a year ago, with the exception of average credit score, which was down slightly in June 2022 (see Figure 6).

Figure 6: Achieve Personal Loans Key Credit Indicators

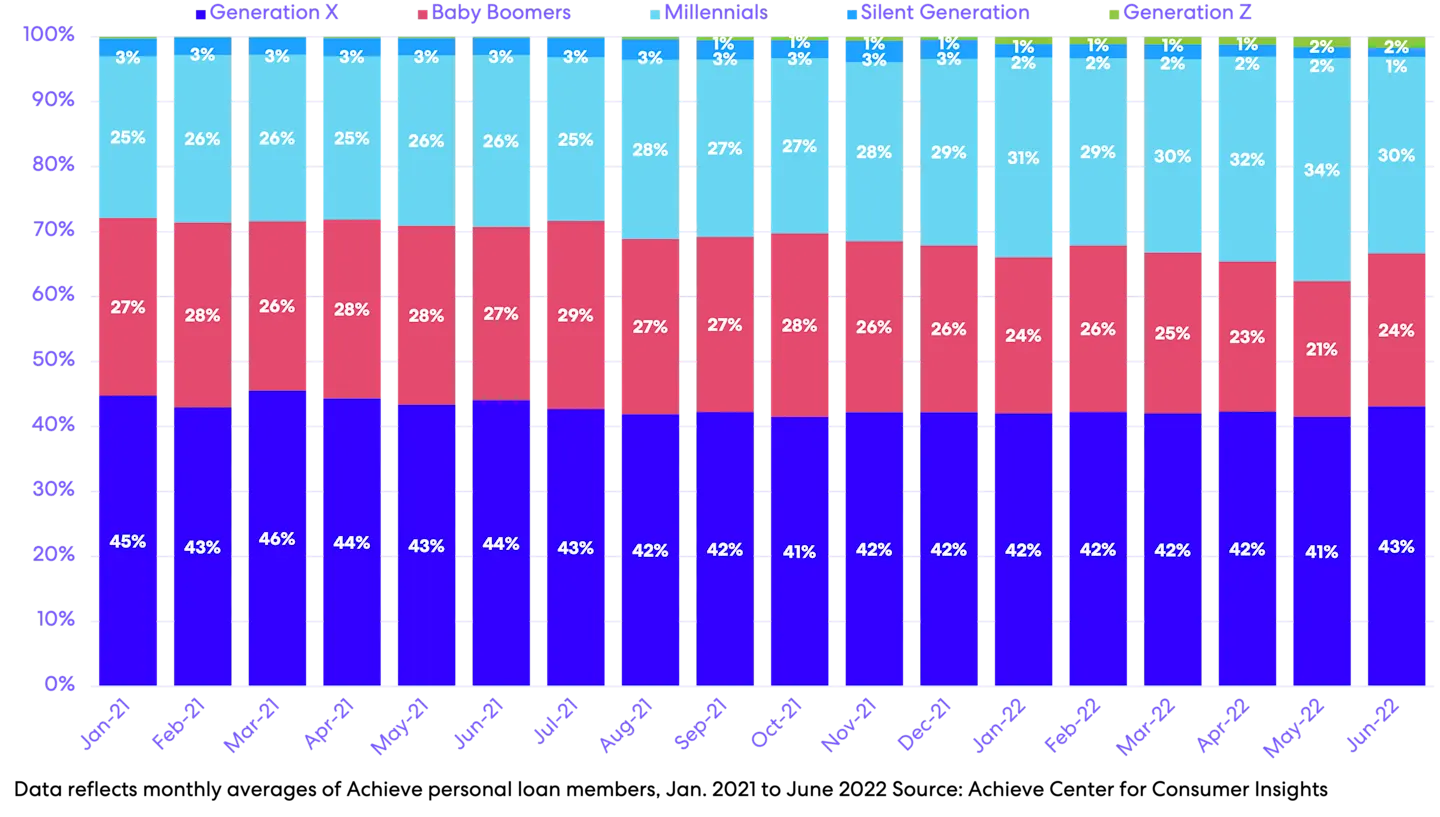

Make Way for Millennials: Millennials represent a growing share of loan volume, and the share of Achieve personal loan members from the Baby Boomer generation is decreasing, mirroring a similar trend in Achieve debt relief. Loans for Gen Z members were nearly nonexistent in 2021, but now account for 2% of transactions in June 2022 (see Figure 7).

Figure 7: Achieve Personal Loans Members, by Generation

Key Findings from Achieve Home Equity Loans

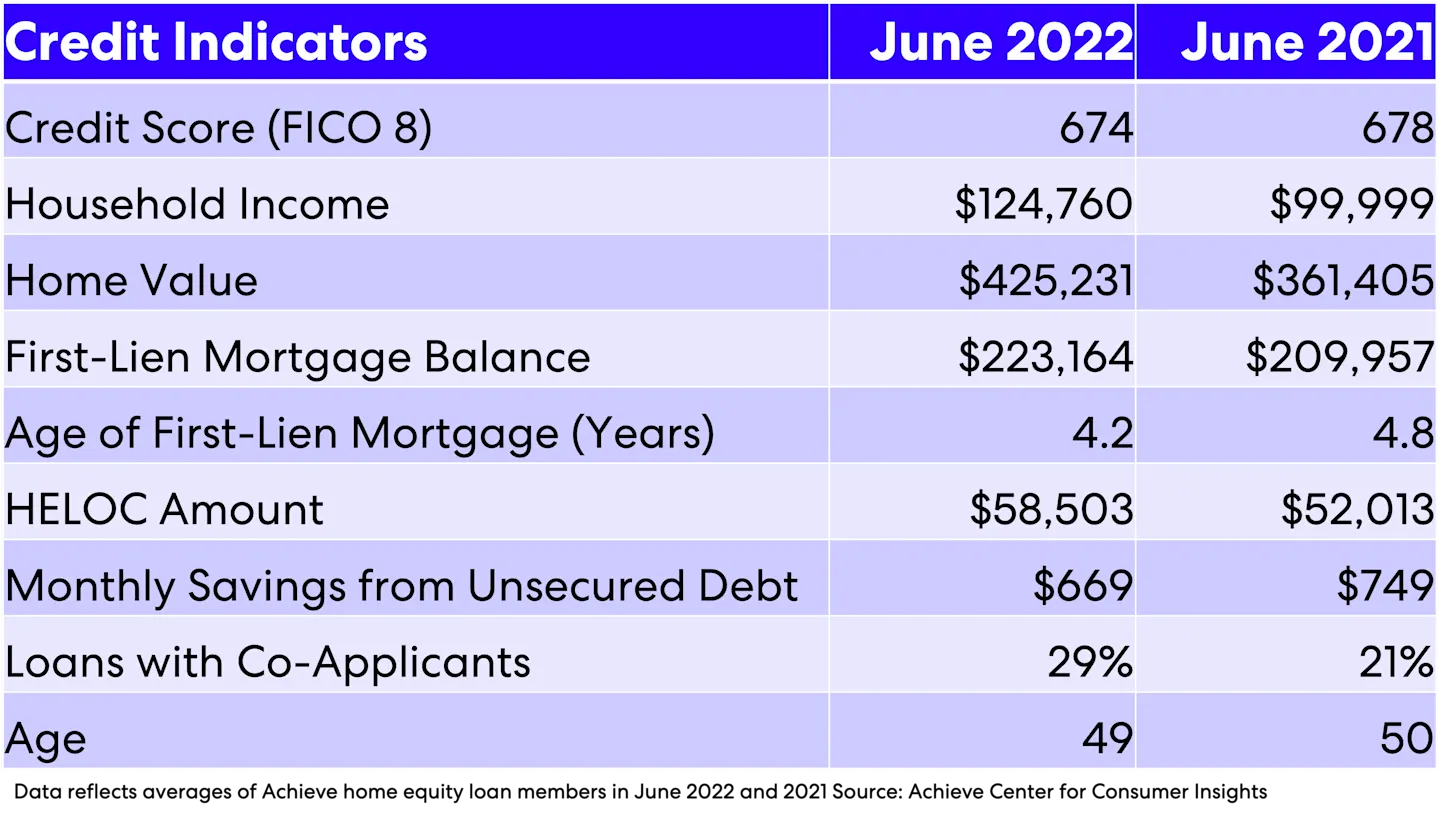

Safely Accessing Home Equity: Members who obtained a home equity loan from Achieve to consolidate unsecured debts in June 2022 save an average of $669 per month compared to their previous monthly debt obligations (see Figure 8).

Achieve’s home equity line of credit (HELOC) program is designed to help borrowers responsibly access equity to pay down debt or grow their cash reserves, without jeopardizing their long-term homeownership goals. Members who obtained a HELOC from Achieve to consolidate their unsecured debts in June 2022 saved an average of $669 per month in payments compared to their previous monthly debt obligations (see Figure 8).

Figure 8: Achieve Home Equity Loan Key Credit Indicators

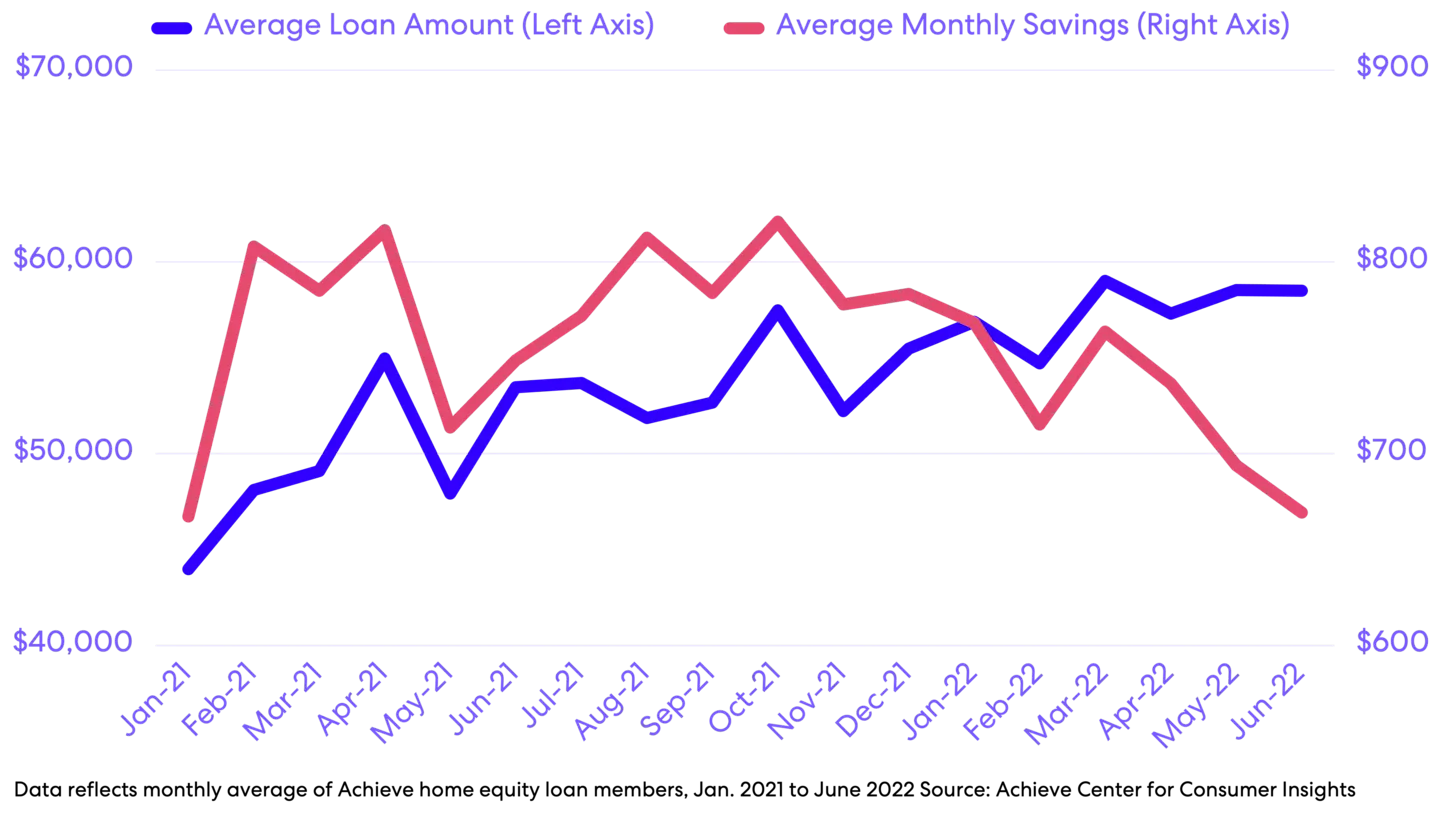

Monthly Savings: Average starting balances of Achieve home equity loans have been between $43,000 and $59,000 from January 2021 to June 2022, with an average starting balance of $55,579 (see Figure 9). Average monthly savings varies over time and by borrower, due to differences in amount of debt, interest rate fluctuations and other individual and market-based factors. Since January 2021, Achieve home equity loan members have reduced their debt payments by an average of $746 per month.

Figure 9: Achieve Home Equity Loans Starting Balance, Monthly Savings

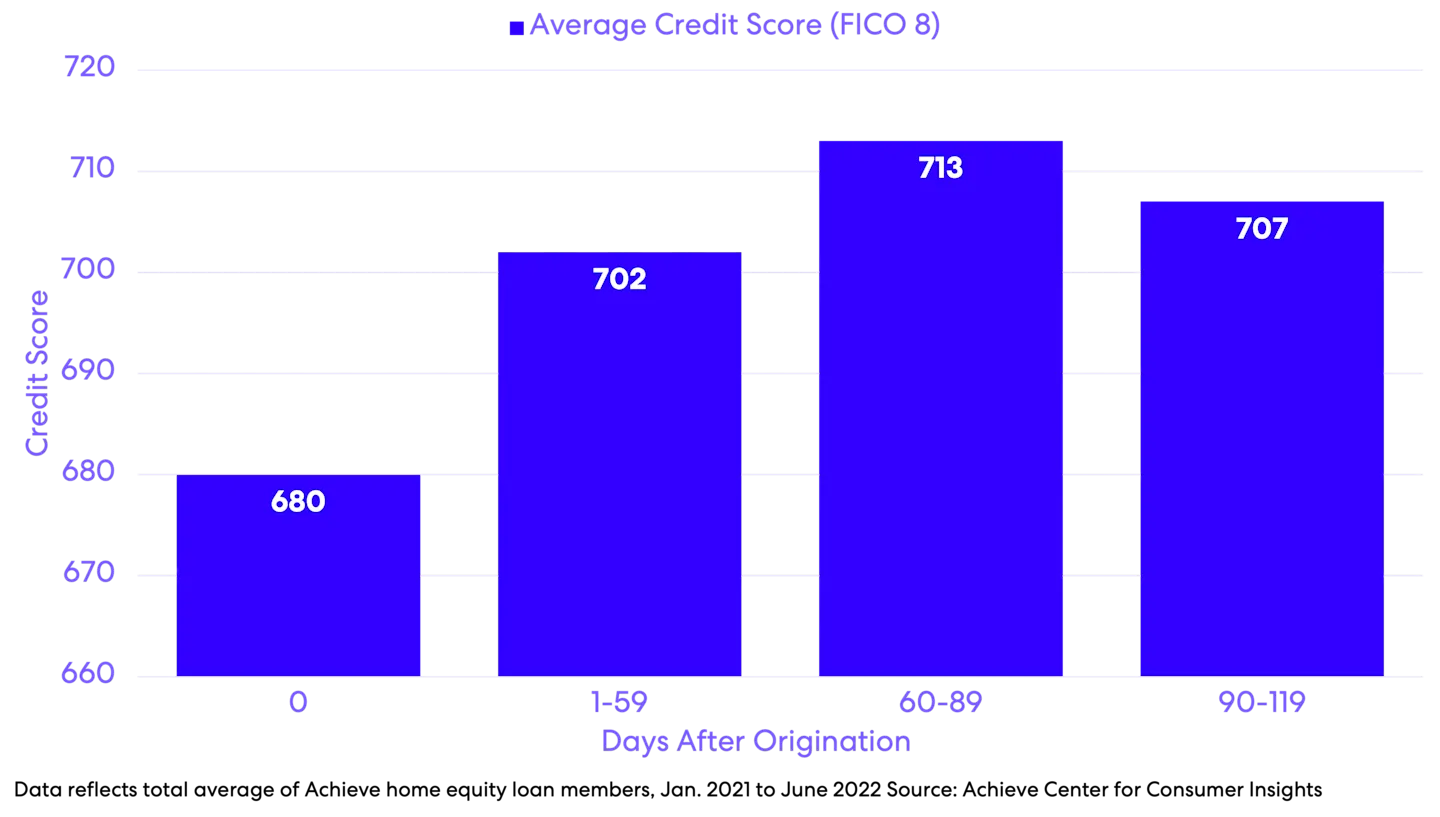

Credit Score Improvement: Members typically see their credit scores increase, in addition to improving their monthly cash flow after consolidating debt with an Achieve home equity loan (see Figure 10). Achieve home equity loans are structured as fixed-rate, fully drawn HELOCs, allowing members to continue to access their home’s equity when needed over the course of the draw period.

Figure 10: Credit Score After Obtaining Achieve Home Equity Loan

About Achieve

Achieve is the leader in digital personal finance. Our solutions help everyday people get on, and stay on, the path to a better financial future, with innovative technology and personalized support. By leveraging proprietary data and analytics, our solutions are tailored for each step of a consumer's financial journey and include personal loans, home loans, help with debt and financial tools and education. Achieve is headquartered in San Mateo, California and has more than 2,700 dedicated employees across the country with hubs in California, Arizona and Texas. The company is regularly recognized as a Best Place to Work.

The data reflected above is based on a representative sample of over 100,000 members who used Achieve debt relief, personal loan and home equity loan offerings from January 2021 to June 2022. The data and findings represents the products and services offered by Achieve and its affiliates, including Bills.com, LLC d/b/a Achieve.com (NMLS ID #138464); Freedom Financial Asset Management, LLC (NMLS ID #227977); Freedom Debt Relief (NMLS ID 1248929); and Lendage, LLC d/b/a Achieve Loans (NMLS ID #1810501).

Buy Now, Pay Later Stretches Limits of Consumer Credit, According to Achieve Center for Consumer Insights Study

3 MB

Contacts

Erica Bigley

VP, Corporate Communications

415-710-9006

Austin Kilgore

Director, Corporate Communications

214-908-5097