Return to Press Room

Till debt do us part: 78% of Americans say a partner with debt is a dating dealbreaker

New study from Achieve shows short-term debt plays a defining role in who Americans are willing to date

February 11, 2026

San Mateo, Calif., Feb. 11, 2026 — While the search for a soulmate often focuses on chemistry and shared interests, a prospective partner’s balance sheet plays a pivotal role in romantic compatibility. Over three-quarters of Americans (78%) are unwilling to be in a relationship with someone who carries short-term debt from credit cards, personal loans and buy now, pay later financing, according to a new survey by Achieve, the leader in digital personal finance.

The 2026 Dating and Debt survey, published by the Achieve Center for Consumer Insights think tank, shows debt has become a front-of-mind factor in modern dating, influencing who people are willing to pursue and commit to.

“With the cost of living still high, many Americans are already under financial pressure,” said Achieve President of Debt Relief Sean Fox. “It’s understandable that people may be cautious about taking on additional debt in a relationship. Open, honest conversations about money can help couples understand each other’s situations and make decisions together.”

Key findings

72% believe couples should discuss debt and their broader financial situation within the first six months of dating.

60% of respondents said they would likely end a relationship if a partner hid debt or spending.

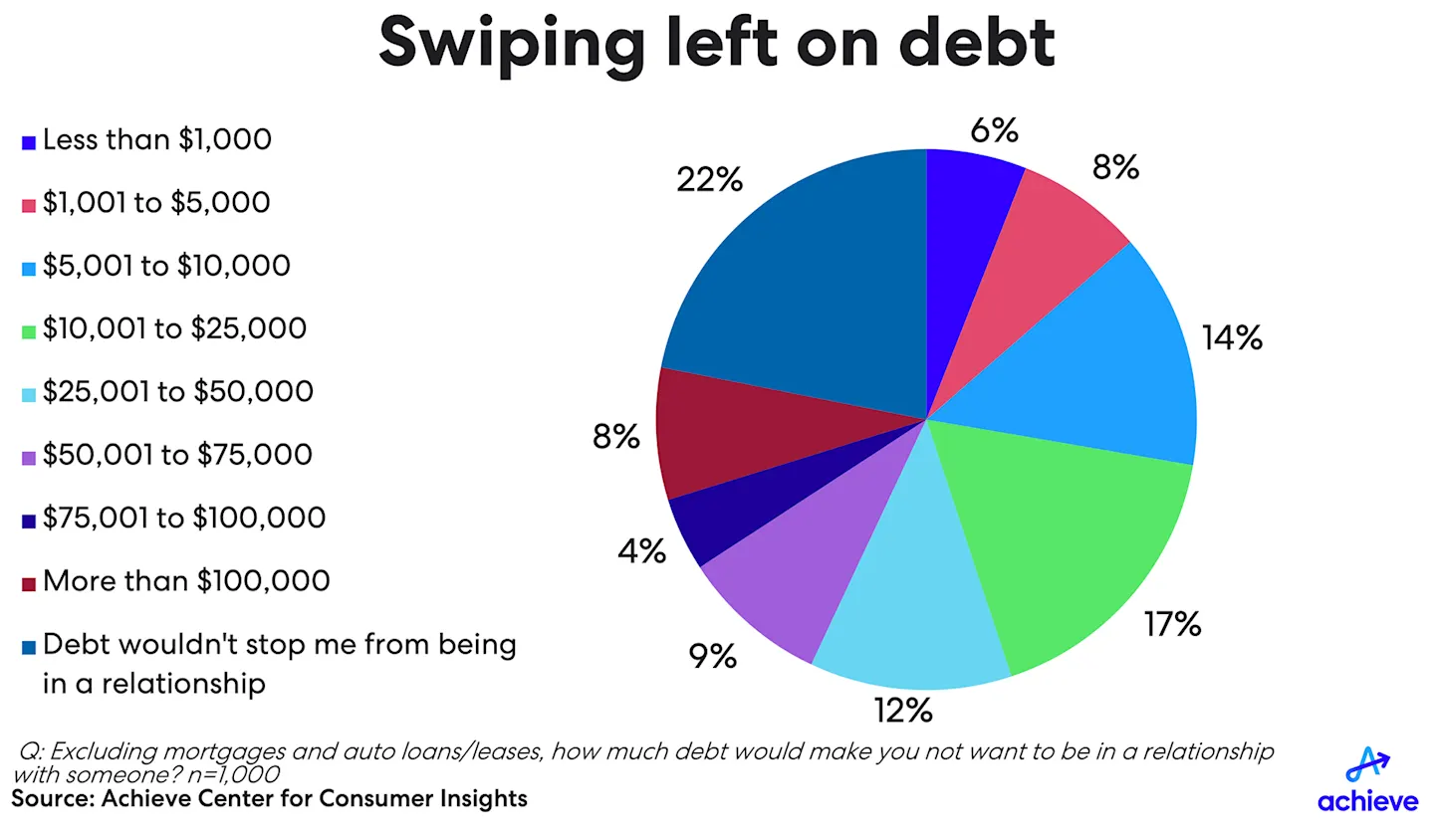

Only 22% claim debt of a potential partner would not stop them from pursuing a relationship.

67% report they would end a relationship if a partner refused to contribute financially.

Debt is a dating dealbreaker for most Americans

American household debt is at a record $18.8 trillion, according to the latest Federal Reserve Bank of New York data, and a recent Achieve study found soaring debt is forcing many consumers to resort to risky stopgaps to make ends meet. But when it comes to relationships, Americans have a surprisingly low tolerance for their partners’ unsecured debt like credit cards, personal loans and buy now, pay later financing.

The survey found 28% of respondents would not want to be in a relationship with someone with $10,000 or less in debt. The threshold for rejection rises quickly from there: nearly half of all consumers (45%) say they would draw the line at $25,000 in debt. With national averages for student loans and credit card balances often exceeding these limits, a significant portion of the dating pool may be unknowingly disqualified before the first date even ends.

Gender and past relationship experience also influences these boundaries. The survey found 74% of men are unwilling to be in a relationship with someone with short-term debt, compared to 80% of women.

Among divorced respondents, 86% are unwilling to date someone with debt, compared to 80% of married people, 76% of singles and 72% of people currently in dating relationships. These differences suggest that people who have already navigated the financial realities of marriage and separation may be more cautious when evaluating a partner’s debt.

Other key findings from the survey:

Couples value honesty: Americans broadly agree on the importance of transparency around money, even as many acknowledge discomfort with sharing financial details at the start of a relationship. About 85% of Americans agree people should be upfront about their debt and spending habits early in a relationship, underscoring how strongly honesty is valued when it comes to finances. While that expectation is widely shared, the study suggests many people still wrestle with how and when to share financial details.

But timing remains a challenge: Views vary on timing, but most believe the conversation should happen relatively early. About 16% said detailed financial information should be shared within the first month of dating, 31% said within one to three months and 25% said within four to six months.

Expectations increase when marriage is part of the picture: About 73% of Americans expect a significant other to pay down debt before getting married. At the same time, 55% said they would be willing to help a partner pay down debt from before the relationship, while 68% said they would not want a spouse or long-term partner to help pay down their own pre-relationship debt.

What the study means for relationships

Taken together, the findings show that debt has moved from a background issue to a defining factor in modern relationships. Financial compatibility, transparency and shared responsibility are now widely viewed as essential to long-term success.

“Money conversations can feel uncomfortable, especially early on,” Fox said. “But this research shows that avoiding them can create far greater strain later. Direct conversations about debt and finances give couples a clearer picture of whether they are truly aligned.”

Methodology

The data and findings presented are based on an Achieve survey conducted in January 2026 consisting of 1,000 U.S. consumers ages 18 and older, and is representative of Census Bureau benchmarks of the U.S. population for age, gender, race and ethnicity.

About the Achieve Center for Consumer Insights

The Achieve Center for Consumer Insights is a think tank that leverages Achieve’s team of digital personal finance experts to provide a view into the state of consumer finances. In addition to sharing insights gleaned from Achieve’s proprietary data and analytics, the Achieve Center for Consumer Insights publishes in-depth research, bespoke data and thoughtful commentary in support of Achieve’s mission of helping everyday people get on the path to a better financial future.

About Achieve

Achieve, THE digital personal finance company, helps everyday people get on, and stay on, the path to a better financial future. Achieve pairs proprietary data and analytics with personalized support to offer personal loans, home equity loans, debt relief and debt consolidation, along with financial tips and education and free mobile apps: Achieve MoLO® (Money Left Over) and Achieve GOOD™ (Get Out Of Debt). Achieve has 2,200 dedicated teammates across the country, with hubs in Arizona, California, Florida and Texas. Achieve is frequently recognized as a Best Place to Work.