Return to Press Room

End of student loan forbearance may create payment shock that spills over to other debts, Achieve warns

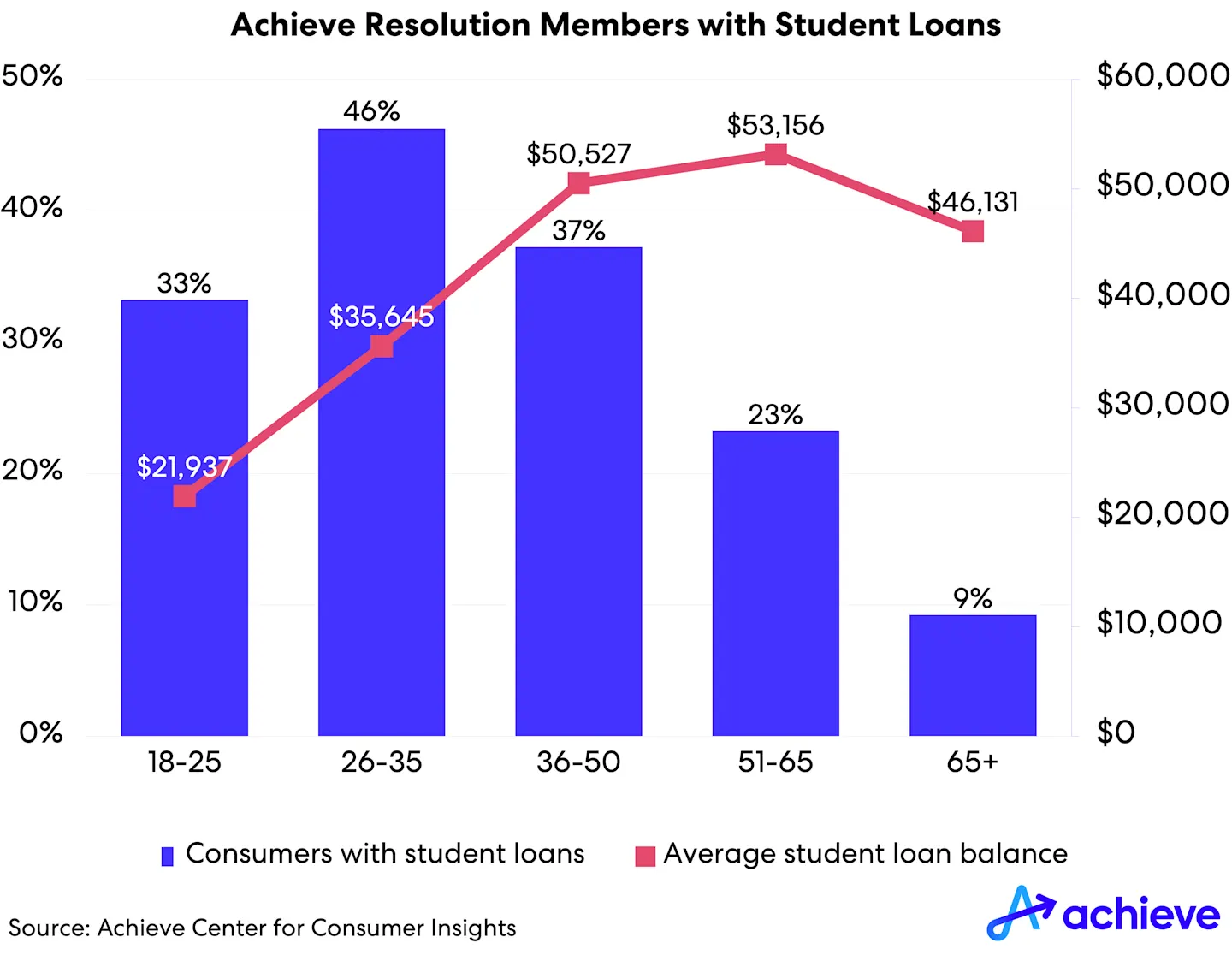

Achieve estimates nearly one in three people seeking debt relief help has an average of $46,000 in student loans. Those figures may rise once borrowers resume student loan payments.

June 27, 2023

SAN MATEO, Calif., June 27, 2023 — With the federal student loan forbearance now set to end on Sept. 1, many Americans – including millions already struggling to make ends meet – will face payment shock when they have to start repaying their loans in October. Achieve, the leader in digital personal finance, found that approximately 30% of members who enrolled in its debt relief program since 2019 have student loan debt. That’s nearly double the estimated 17% of the U.S. adult general population who have federal student loan debt.

What’s more, the amount of student debt held by Achieve’s debt relief members is significant, averaging $46,000 per borrower, according to an analysis of credit data from consumers who enrolled in the Achieve Debt Relief program from January 2019 to May 2023. The analysis shows that Americans between the ages 26 and 35 were most likely to have open student loan accounts, followed by those between the ages 36 and 50. Meanwhile, consumers who enrolled in Achieve’s debt relief program between the ages 51 and 65 had the largest student loan balances.

“Millions benefited from the federal student loan forbearance that was put in place during the pandemic to help Americans cope with the economic uncertainty brought on by COVID-19,” explained Andrew Housser, Co-Founder and Co-CEO of Achieve. “Today, the rising costs of groceries, gas, childcare and other everyday expenditures, combined with rising interest rates, means that more people have expenses that exceed their income. It’s also becoming harder to secure loans to help bridge the gap.”

Student loan debt is often framed as a financial challenge for Millennial and Generation Z consumers. However, the large student loan balances held by Generation X and Baby Boomer consumers enrolled in Achieve Debt Relief highlight the reality that many parents and grandparents cosign student loans for children and other family members. Cosigners are not primarily responsible for repaying loans, but their credit profile can be negatively affected by late or missed payments and defaults.

Many Americans are already living close to the edge with their finances. Achieve’s recent “Financial Fit Check” study showed that 66% of American adults are living paycheck to paycheck. Just over half of respondents (51%) have less than $1,000 in an emergency savings fund, including 28% who said they have no emergency savings at all. With student loan forbearance coming to an end, even more people will feel the effects of greater financial stress.

A recent CFPB study found that more than one-in-thirteen student loan borrowers are currently behind on their other payment obligations and about one-in-five student loan borrowers have risk factors that suggest they could struggle when scheduled payments resume.

Programs like Achieve Debt Relief can help consumers reduce the amount they owe on credit cards, buy now, pay later accounts, medical bills, personal loans and other types of unsecured debt. However, this typically does not include student loans. Likewise, most student loans can’t be discharged in bankruptcy. This makes it difficult for consumers struggling with student loans and other types of debt to get back on track.

“Rising consumer debt is jeopardizing people’s mental and physical health,” said Housser. “While the federal student loan forbearance was critical to the economic response to the pandemic, further reforms are needed to help consumers better manage this significant financial burden.”

For those struggling to make ends meet, Achieve offers a variety of digital personal finance help. In addition to the Achieve Debt Relief program, Achieve can help consumers obtain a personal loan or home equity line of credit (HELOC) to consolidate debts. In May, the company launched its free Achieve MoLO app, which helps create a monthly budget, categorize spending, and even make recommendations to reduce non-essential spending to increase the amount of money left at the end of each month.

About Achieve

Achieve is the leader in digital personal finance. Our solutions help everyday people get on, and stay on, the path to a better financial future, with innovative technology and personalized support. By leveraging proprietary data and analytics, our solutions are tailored for each step of a consumer’s financial journey and includepersonal loans,home equity loans andhelp with debt. In addition, Achieve also providesfinancial tips andeducation, including a free specialized mobile app,MoLO (Money Left Over). Headquartered in San Mateo, California, Achieve has nearly 3,000 dedicated teammates across the country with hubs in California, Arizona, Texas and Florida. Achieve is frequently recognized as a Best Place to Work.

Achieve and its affiliates are subsidiaries of Freedom Financial Network Funding, LLC, including Bills.com, LLC d/b/a Achieve.com (NMLS ID #138464) Equal Housing Lender; Freedom Financial Asset Management, LLC d/b/a Achieve Personal Loans (NMLS ID #227977); Freedom Debt Relief (NMLS ID #1248929); and Lendage, LLC d/b/a Achieve Loans (NMLS ID #1810501), Equal Housing Lender.

Contacts

Erica Bigley

Vice President, Corporate Communications

415-710-9006

Austin Kilgore

Director, Corporate Communications

214-908-5097