Return to Press Room

Inflation, lost wages and forgetting to pay: Achieve survey examines why American households are drowning in debt

First-of-its kind research from Achieve offers qualitative insights on why household debt and credit is growing at an unsustainable pace.

May 13, 2024

TEMPE, Ariz., May 13, 2024 — Amid a well-documented surge in both consumer debt and loan delinquencies, few Americans are optimistic about their current financial situation. Many point to rising debt and difficulty living within their means as the main culprits, according to a first-of-its-kind report from Achieve, the leader in digital personal finance.

Achieve’s think tank, the Achieve Center for Consumer Insights, surveyed 2,000 consumers with active accounts across six categories of consumer debt, including credit cards, mortgages and home equity lines of credit, auto and student loans. The survey format and respondent panel are designed to complement the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit by providing qualitative insights into consumer borrowing trends. To further examine the causes and ramifications of rising loan delinquencies, the survey panel includes a subset of borrowers who were 30 days’ or more past due at least once during the past six months.

“Every month, Achieve teammates support thousands of consumers who are struggling with debt and looking for help to get back on track,” said Achieve Co-Founder and Co-CEO Andrew Housser. “We know that household debt and credit are growing at an alarming pace. Skipping payments on financial obligations in order to afford essentials is the type of decision driving more everyday people deeper into debt. This research highlights the choices that many consumers have to make month after month to simply stay afloat.”

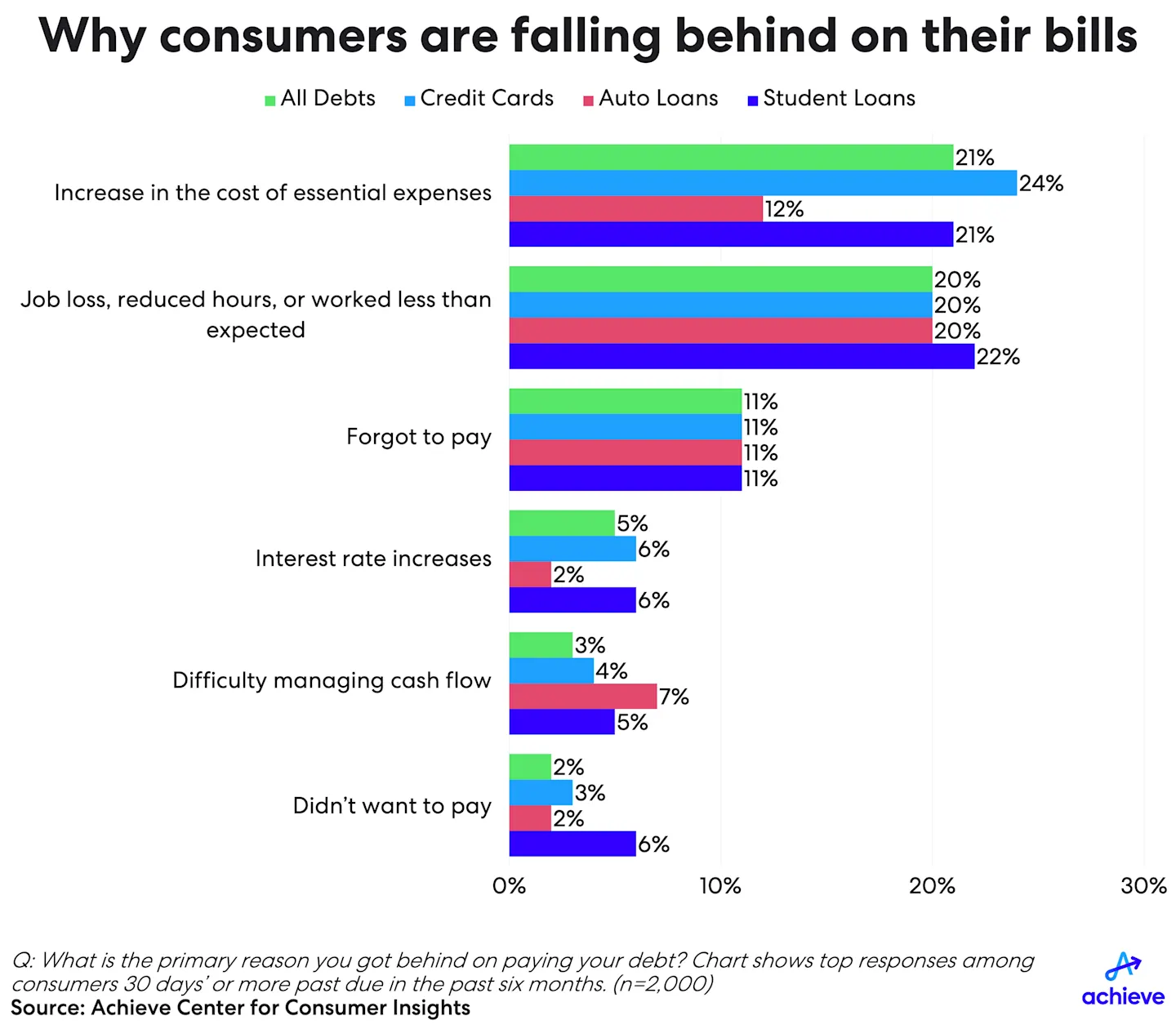

High prices, low wages force tough choices

Consumers with a delinquency on any account in the past six months pointed to a number of reasons they got behind on their payments, including the impact of inflation on essential expenses (21%), a reduction in work and income (20%) and forgetting to pay (11%). In addition, consumers with a recent credit card delinquency said interest rate increases (6%) made paying difficult, while delinquent auto loan borrowers cited difficulty managing cash flow between when respondents receive income and their payment due dates (7%). In student loans, 6% of delinquent borrowers said they missed a payment because they didn’t want to pay.

Why consumers struggle to pay their bills on time

Nearly one-third of consumers (31%) said it is very difficult or difficult for them to pay their recurring debts on time. Among these respondents, 65% said it simply comes down to not having enough income to cover their spending. Other challenges include owing money on too many different accounts (39%); cash flow timing differences between when income is received and debt payments are due (27%) and difficulty keeping track of how much is owed across all their accounts (14%).

“For many consumers, money is going out the door as quickly as it’s coming in, if not faster,” Housser said.

Consumers often face difficult choices when struggling to make ends meet. Over the past three months, 25% of survey respondents said they have reduced spending on basic needs; 18% have taken on additional credit card debt and 11% report skipping payments on one or more of their bills.

From delinquency to debt spiral

Achieve’s research shows how consumers who are delinquent on one of their accounts are significantly more likely to be behind on other debts as well. For example, among respondents delinquent on a major credit card in the past six months, 23% were also delinquent on store-branded credit cards; 17% on buy now, pay later loans; and 28% on unsecured personal loans. Contrast that with credit card borrowers who are current on their accounts, where delinquencies on their other consumer debts are 1% to 2%.

For many consumers, having multiple bills due at once is another source of financial strain, both in terms of struggling to have money to make on-time payments and the complexity of managing a portfolio of accounts. This is especially true in light of the growing popularity of buy now, pay later (BNPL) loans. A recent Achieve Center for Consumer Insights study on buy now, pay later lending found that once consumers make a purchase using BNPL, they’re likely to use it again. Consumers who make a habit out of using BNPL can quickly find themselves managing numerous transactions, often owing payments to multiple different lenders.

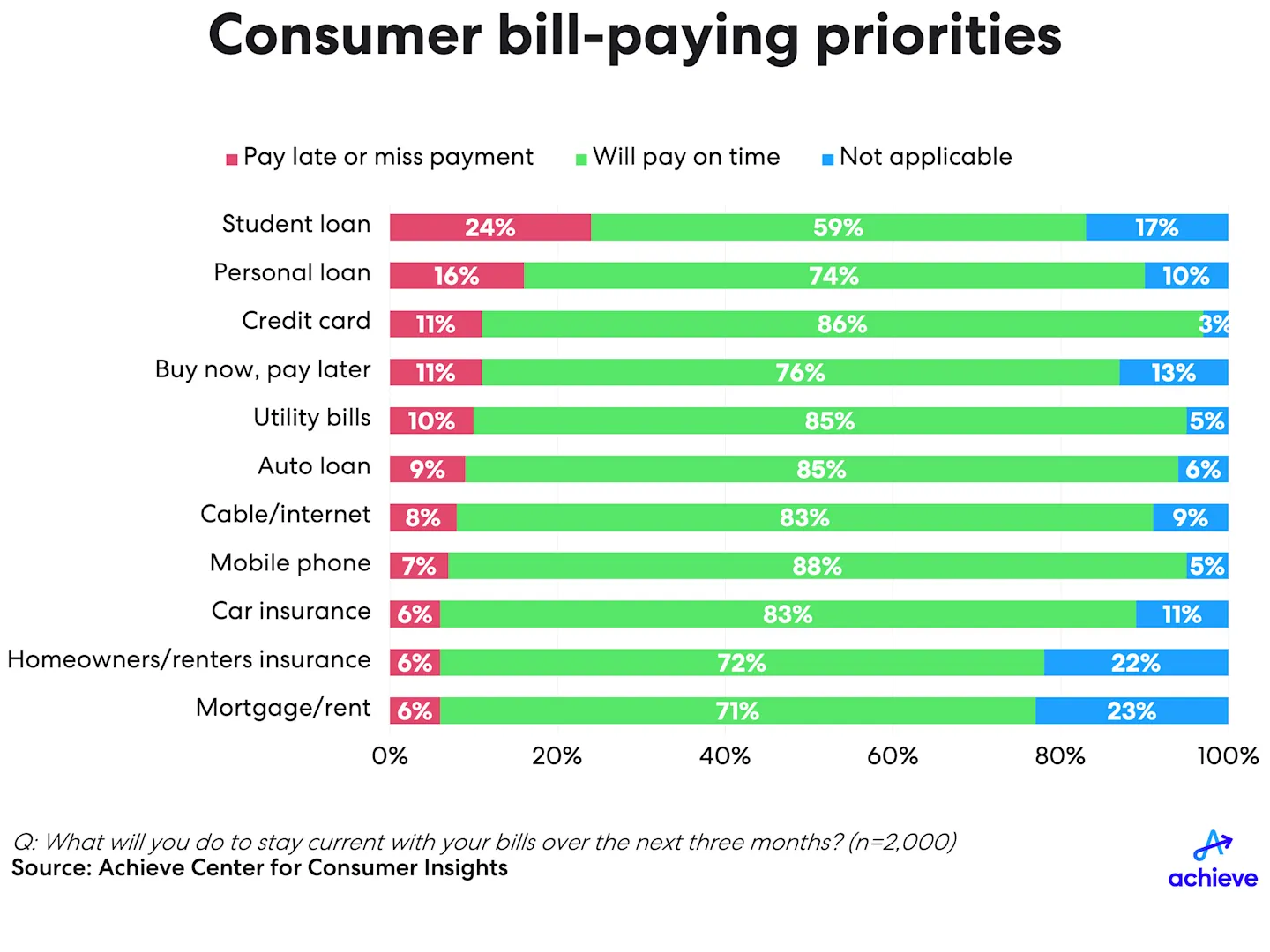

Nearly one-in-four expect to struggle with student loans

Looking ahead to the next three months, a majority of respondents expect to pay all of their bills on time. But Achieve’s research also reveals which debts and bills will take precedence among those struggling with their household finances. Consumers said they are most likely to be late or skip their personal and student loan payments and stay on time with their mobile phone, mortgage/rent and homeowners or renters insurance payments. Respondents also said the bills most likely to go unpaid include student loans (24%), personal loans (16%) and buy now, pay later loans (11%).

“Whether student loan borrowers don’t have enough money to pay all of their bills or they’re waiting to see if more debt forgiveness will be approved in Washington, it’s clear that other debts are taking precedence,” said Housser. “This data shows why the inability to enroll student loans in a debt relief program or get them discharged in bankruptcy is an outdated and ineffective policy that does little to deter loan defaults.”

Methodology

The data and findings presented are based on an Achieve survey conducted in April 2024 consisting of 2,000 U.S. consumers ages 18 and older with an active account for one or more of the following categories of consumer debt: auto loan; major credit card with a minimum outstanding balance of $100; first-lien mortgage; home equity line of credit (HELOC); student loan; and other (unsecured personal loan; store-branded credit card; buy now, pay later loan; closed-end home equity loan). The sample was augmented to include a statistically significant subset of credit card, auto loan and student loan borrowers who have been 30 days’ or more past due at least once in the past six months.

About the Achieve Center for Consumer Insights

The Achieve Center for Consumer Insights is a think tank that leverages Achieve’s team of digital personal finance experts to provide a view into the state of consumer finances. In addition to sharing insights gleaned from Achieve’s proprietary data and analytics, the Achieve Center for Consumer Insights publishes in-depth research, bespoke data and thoughtful commentary in support of Achieve’s mission of helping everyday people get on the path to a better financial future.

About Achieve

Achieve, THE digital personal finance company, helps everyday people get on, and stay on, the path to a better financial future. Achieve pairs proprietary data and analytics with personalized support to offer personal loans, home equity loans, debt relief and debt consolidation, along with financial tips and education and a free mobile apps Achieve MoLO (Money Left Over). Achieve has 2,500 dedicated teammates across the country with hubs in Arizona, California, Florida and Texas. Achieve is frequently recognized as a Best Place to Work.

Achieve refers to the global organization and may denote one or more affiliates of Achieve Company, including Achieve.com (NMLS ID #138464); Achieve Home Loans, Equal Housing Lender (NMLS ID #1810501); Achieve Personal Loans (NMLS ID #227977); Freedom Debt Relief (NMLS ID # 1248929) and Freedom Financial Asset Management (CRD #170229).

Contacts

Contacts

Erica Bigley

Vice President

Corporate Communications

415-710-9006

Austin Kilgore

Director

Corporate Communications

214-908-5097