At Achieve, we're committed to providing you with the most accurate, relevant and helpful financial information. While some of our content may include references to products or services we offer, our editorial integrity ensures that our experts’ opinions aren’t influenced by compensation.

Achieve Insights

Rising debt is taking a toll on Americans’ financial and mental health

May 14, 2026

Written by

Key takeaways:

Debt isn’t just high — it’s growing: Nearly a third of respondents say their unsecured debt increased over the past 12 months, and 34% say they are unable to make the full monthly payment on all their debts. Borrowers whose debt increased in the past year report worse outcomes across most major measures.

Money issues can take a major emotional toll: Around half of respondents report trouble sleeping (49%), feeling anxious or on edge (50%), or feeling overwhelmed (44%).

Some consumers cope in risky ways: One in five say they use alcohol or other substances to cope with financial stress, and 14% have delayed or skipped medical treatment because of money.

Most respondents are looking for solutions: More than half of respondents (53%) say their household’s finances “need a strategic reset.” The share spikes to eight out of 10 respondents who feel they have too much debt.

Debt has become a public health crisis.

As Americans pay more for housing, utilities, groceries, gas and health care, many are taking on more debt to cover their needs — a burden that roughly a third say is unmanageable, according to a new survey from Achieve and Money.com.

In some cases, the strain is pushing borrowers to make risky moves to try to make ends meet, such as forgoing medical treatment or tapping their retirement savings. The pressure of paying off those loans is taking a toll on their mental and physical health, as well as their bank accounts. But the survey also suggests many borrowers want to turn their finances around, and they’re open to several repayment strategies that could help.

“The data shows that for many everyday people, debt has moved beyond a financial hurdle and is now a pervasive health issue,” said Achieve Co-Founder and Co-CEO Brad Stroh. “When 80% of those with unmanageable debt are unable to meet their monthly obligations, it is clear that the traditional path is no longer working. There is a profound need for a strategic reset in how households approach their financial journeys.”

Debt is growing — and getting harder to manage

Only a third of Americans are living debt-free today. While many feel they have a handle on what they owe, a significant and growing share report that their balances have climbed over the past year — and the more debt people carry, the less in control they tend to feel.

Even respondents who currently feel in control aren’t immune. Nearly 4 in 10 of them still saw their unsecured balances grow in the past year, suggesting that rising costs are putting pressure on households across the board — not just those already in distress.

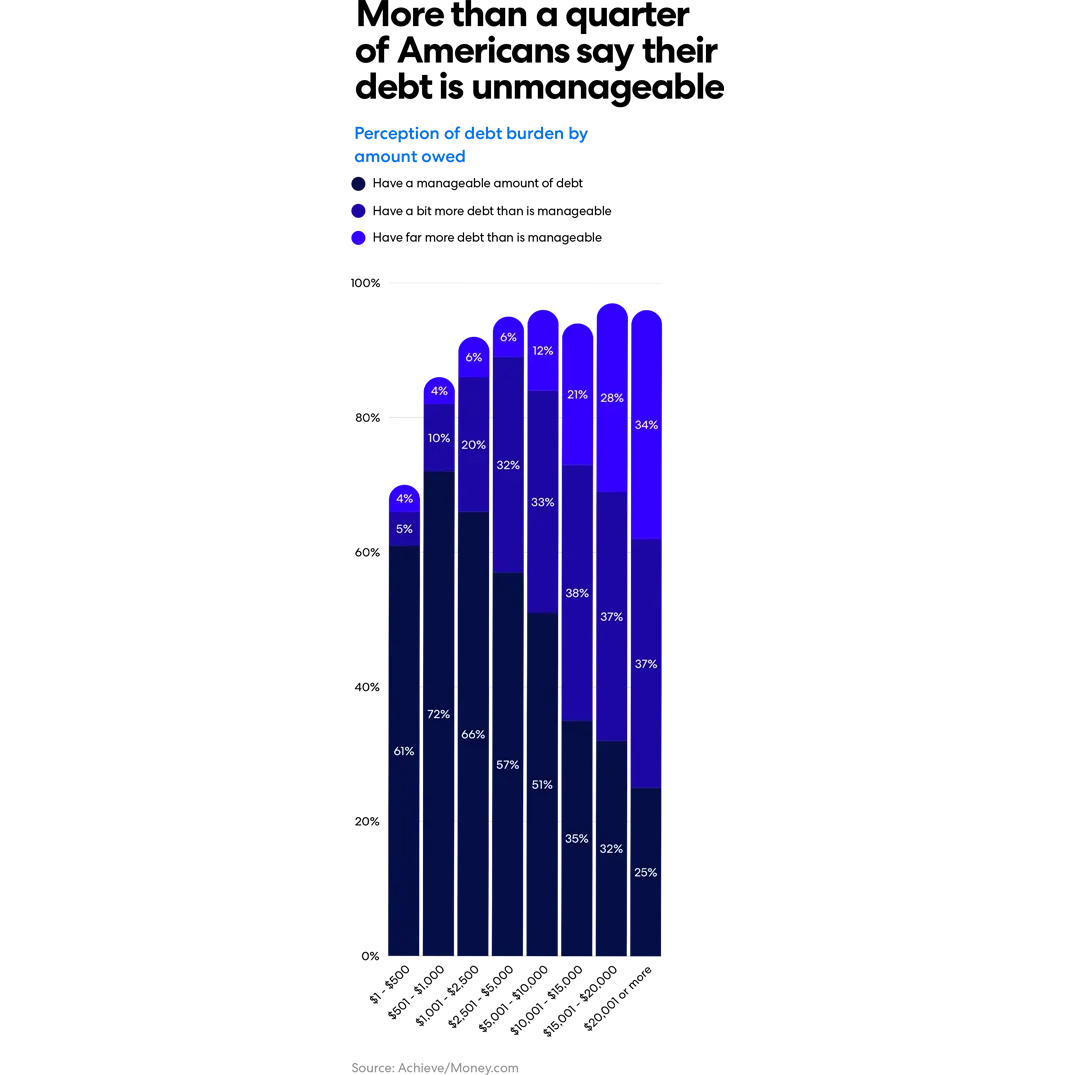

More than a quarter of Americans say their debt is unmanageable

Only a third of consumers are living debt-free, according to the survey findings. But many with debt do feel they’re able to control it: 42% of respondents report they have a manageable amount of debt. (The survey asked about how respondents perceived their debt load, not just the dollar amount they owed.)

But there is a significant minority of Americans who are struggling to stay on top of their debt: 18% of respondents feel they have a bit more debt than is manageable, and 10% say they have far more than is manageable. Typically, the more unsecured debt — a line of credit or loan not backed by collateral, including credit cards and personal loans — the less likely a borrower feels like they’re in control.

Still, as costs surge even respondents who feel like they have a handle on their debt are watching their balances climb, with 39% indicating that their unsecured debt increased over the past year.

Financial anxiety bleeds into all aspects of life

Financial troubles don’t just hurt wallets. Respondents say thinking about money has taken a toll on their mental and physical health in the last year, too.

About half have felt anxious (50%), depressed (46%) or overwhelmed (44%). Experiencing shame was common, too, with 39% saying they felt embarrassed and 43% saying they felt hopeless about their financial situation.

Those negative emotions ripple into all parts of life: Nearly half of respondents say they’ve had trouble sleeping and a quarter report intimacy challenges with their partner connected to their finances.

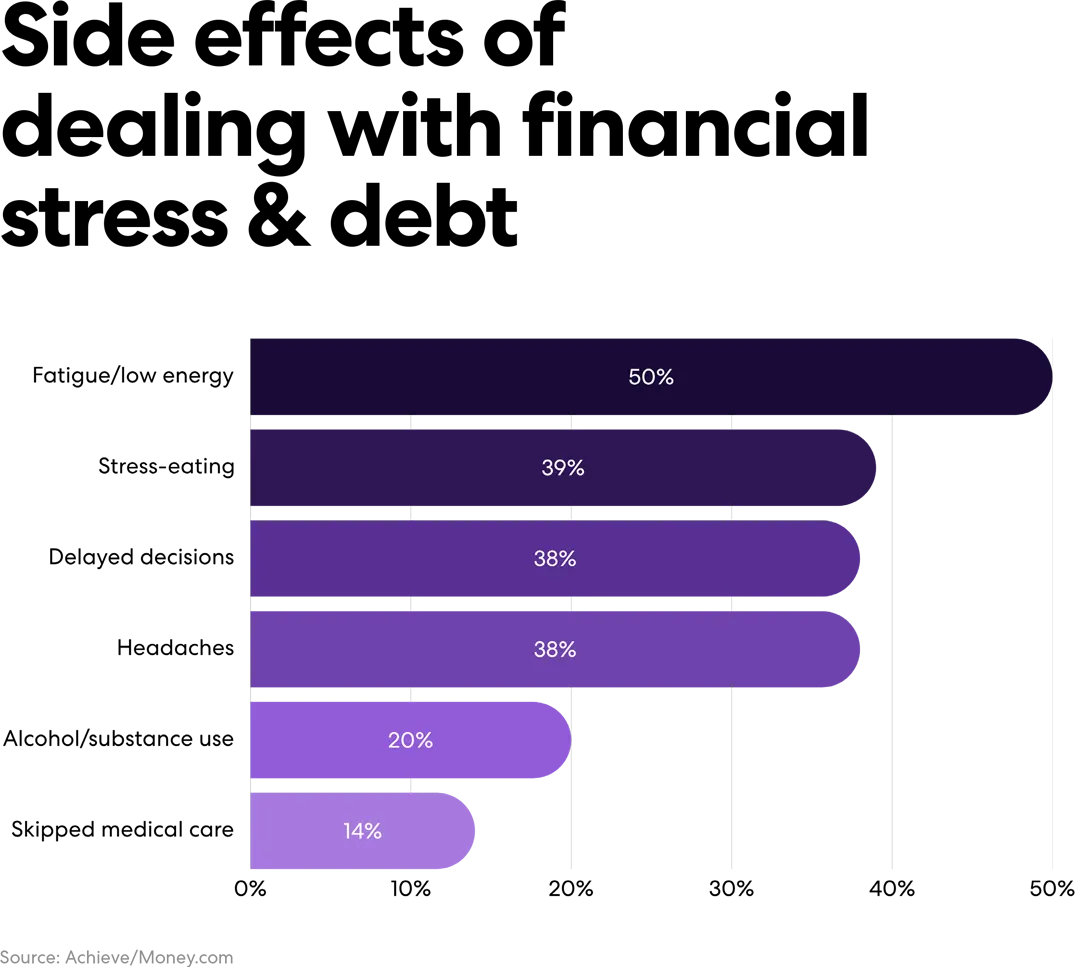

Side effects of dealing with financial stress & debt

More debt tends to cause more strain. Respondents whose debt has risen in the last year show consistently worse financial stress indicators across nearly every measure. The clearest dividing line, though, is whether respondents feel their debt is manageable.

Sleep trouble, anxiety and other signs of distress jump for borrowers who say they have far more debt than is manageable. Many respondents report coping in ways that could have long-term consequences.

These findings suggest financial stress is not just emotional. It can also affect consumers’ health and decision-making.

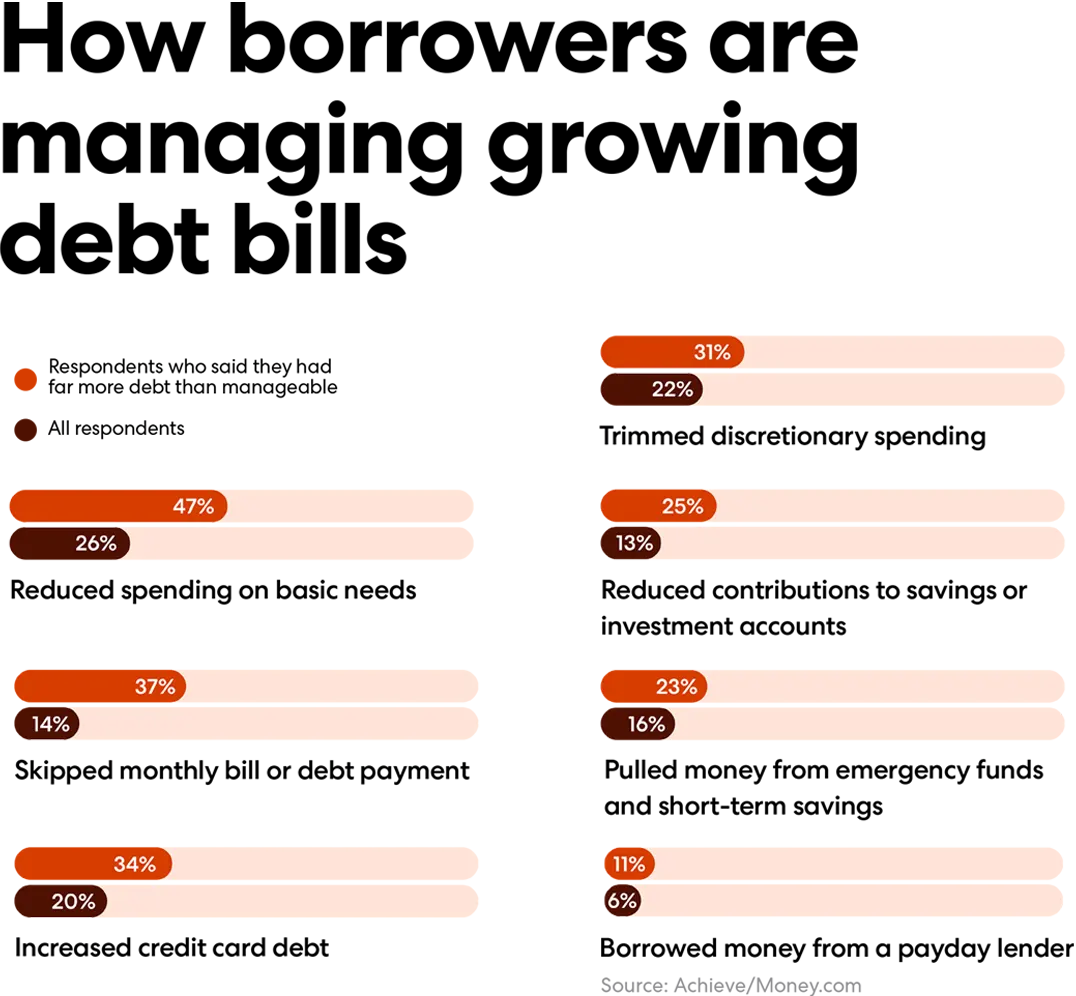

How borrowers are managing growing debt bills

The more debt a consumer feels they have, the more difficult it is for them to make their full monthly payments on their loans. While 34% of all respondents say they’re unable to pay

in full each month, 57% of those who have “a bit more debt than manageable” and 80%

of those with “far more debt than is manageable” say the same. Borrowers whose debt increased in the past year were also more likely to report missing payments. The pattern suggests a compounding cycle: Rising balances make it harder to keep up and falling behind on payments pushes balances even further as interest accrues.

Some respondents have had to cut back on spending while others are making precarious moves because they haven’t been able to pay.

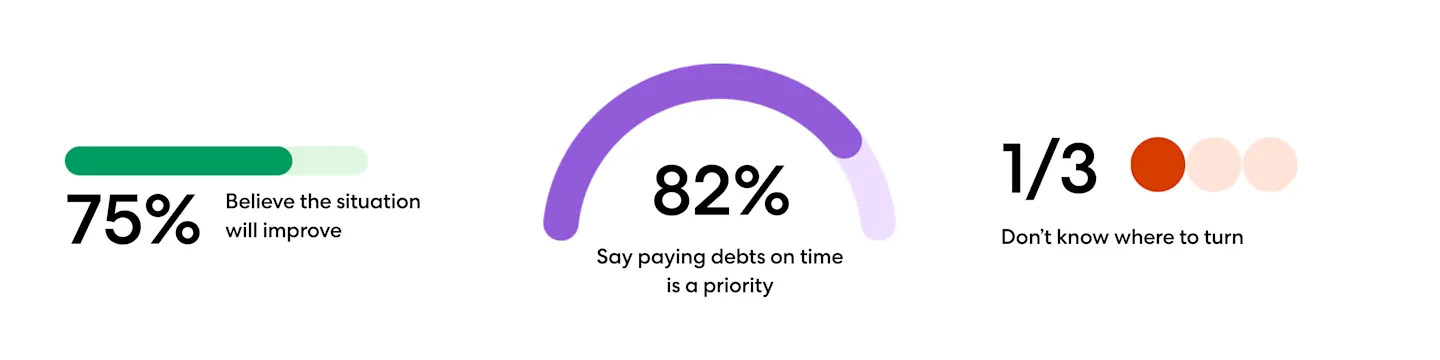

Still, borrowers are hoping to get back on track: 82% of respondents say paying debts on time is a priority for their household, and 75% indicated that they remain hopeful their financial situation will improve over the next few years.

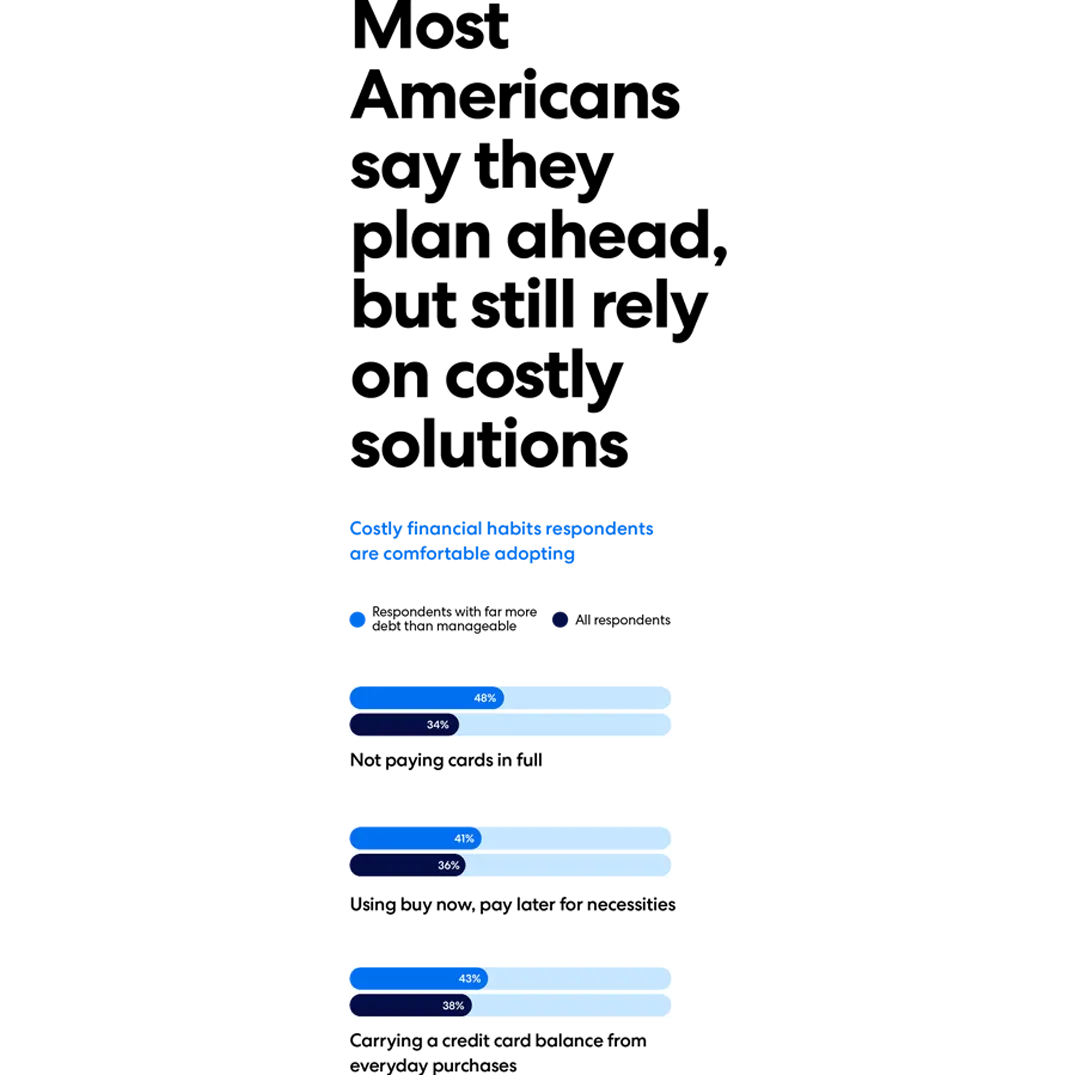

Most Americans say they plan ahead, but still rely on costly solutions

Nearly three-fourths of respondents say their household plans ahead financially. But many are still comfortable relying on tools that can make loans harder to pay off over time, especially when their debt already feels unmanageable.

Carrying a credit card balance from one month to the next (which often comes with an interest rate of more than 20%) and using “buy now, pay later” financing might occasionally be necessary to help consumers cover short-term budget challenges. But they can also make it harder to reduce balances over time, potentially trapping consumers in a cycle of expensive debt.

Many want a financial ‘reset’ but aren’t sure where to turn

82% Say paying debts on time is a priority

75% Believe the situation will improve

33% Don’t know where to turn

“It is important to recognize there is no one-size-fits-all approach to debt, as the path to financial health is a deeply personal process, because every person’s journey is different, we believe the most effective path forward is one tailored to an individual’s unique needs and long-term goals,” Stroh said.

The less manageable borrowers feel their debt is, the harder it becomes for many to make their full monthly payments. Roughly a third of respondents say they don’t know where to turn when they’re looking for help with their money, and around one in four say they face uncertainty or confusion about making the right financial decisions. At the same time, many are looking to turn things around: More than half (53%) of Americans say their household’s finances need a strategic reset.

Most respondents are comfortable turning to mainstream tools and strategies. But significantly less would be ready to implement more aggressive relief options, such as those that could hurt their credit scores.

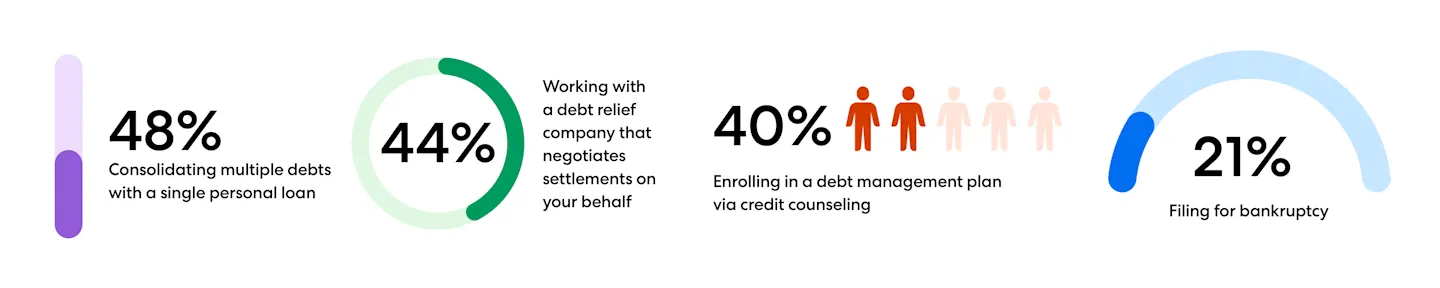

Debt repayment strategies consumers would consider using

48% Consolidating multiple debts with a single personal loan

44% Working with a debt relief company that negotiates settlements on your behalf

40% Enrolling in a debt management plan via credit counseling

21% Filing for bankruptcy

Consumers are most open to strategies that simplify or speed up repayment. Nearly half would consider consolidating debt into a single loan or using savings to pay down high-interest balances, while many are also willing to seek help through negotiation services or credit counseling plans. Balance transfer credit cards remain a common option.

Methodology

The data presented are based on a joint Achieve and Money.com survey fielded in February 2026. The respondent sample consisted of 2,000 U.S. consumers ages 18 and older who identified as being either the primary or shared financial decision-maker in their household.

Author Information

Written by

Achieve is the leader in digital personal finance. Money.com, a digital destination, helps create richer lives for everyone—in every sense of the word.

Related Articles

Americans in their 20s and 30s are becoming seriously delinquent on their credit cards at a faster pace than before the pandemic and approaching levels not seen since the Great Recession.

On the surface, the premise of Buy Now, Pay Later is simple and appealing. But borrowers who can’t afford to repay their BNPL loans risk getting hit with late fees, falling behind on other financial obligations, damaging their credit and other challenges.

With financial volatility on the rise, it’s time to rethink how people use mobile apps to manage their money

Americans in their 20s and 30s are becoming seriously delinquent on their credit cards at a faster pace than before the pandemic and approaching levels not seen since the Great Recession.

On the surface, the premise of Buy Now, Pay Later is simple and appealing. But borrowers who can’t afford to repay their BNPL loans risk getting hit with late fees, falling behind on other financial obligations, damaging their credit and other challenges.

With financial volatility on the rise, it’s time to rethink how people use mobile apps to manage their money