At Achieve, we're committed to providing you with the most accurate, relevant and helpful financial information. While some of our content may include references to products or services we offer, our editorial integrity ensures that our experts’ opinions aren’t influenced by compensation.

Achieve Insights

How consumers can get over-extended using Apple Pay Later and other BNPL loans

Apr 11, 2023

Written by

On the surface, the premise of Buy Now, Pay Later (BNPL) is simple and appealing: interest-free loans repaid over a short period of time that allow consumers to finance purchases right at merchants’ digital or physical point of sale. But interest-free debt is still debt, and borrowers who can’t afford to repay their BNPL loans risk getting hit with late fees, falling behind on other financial obligations, damaging their credit and other challenges.

With Apple poised to put its new Apple Pay Later offering in the pockets of the roughly 125 million iPhone users in the United States, use of BNPL financing is likely to continue to grow. But cracks are emerging in the BNPL market at a time when rising inflation is putting a strain on household balance sheets and the risk of a recession looms large. A recent study by the Consumer Financial Protection Bureau found “BNPL borrowers were, on average, much more likely to be highly indebted, revolve on their credit cards, have delinquencies in traditional credit products, and use high-interest financial services such as payday, pawn, and overdraft compared to non-BNPL borrowers.”

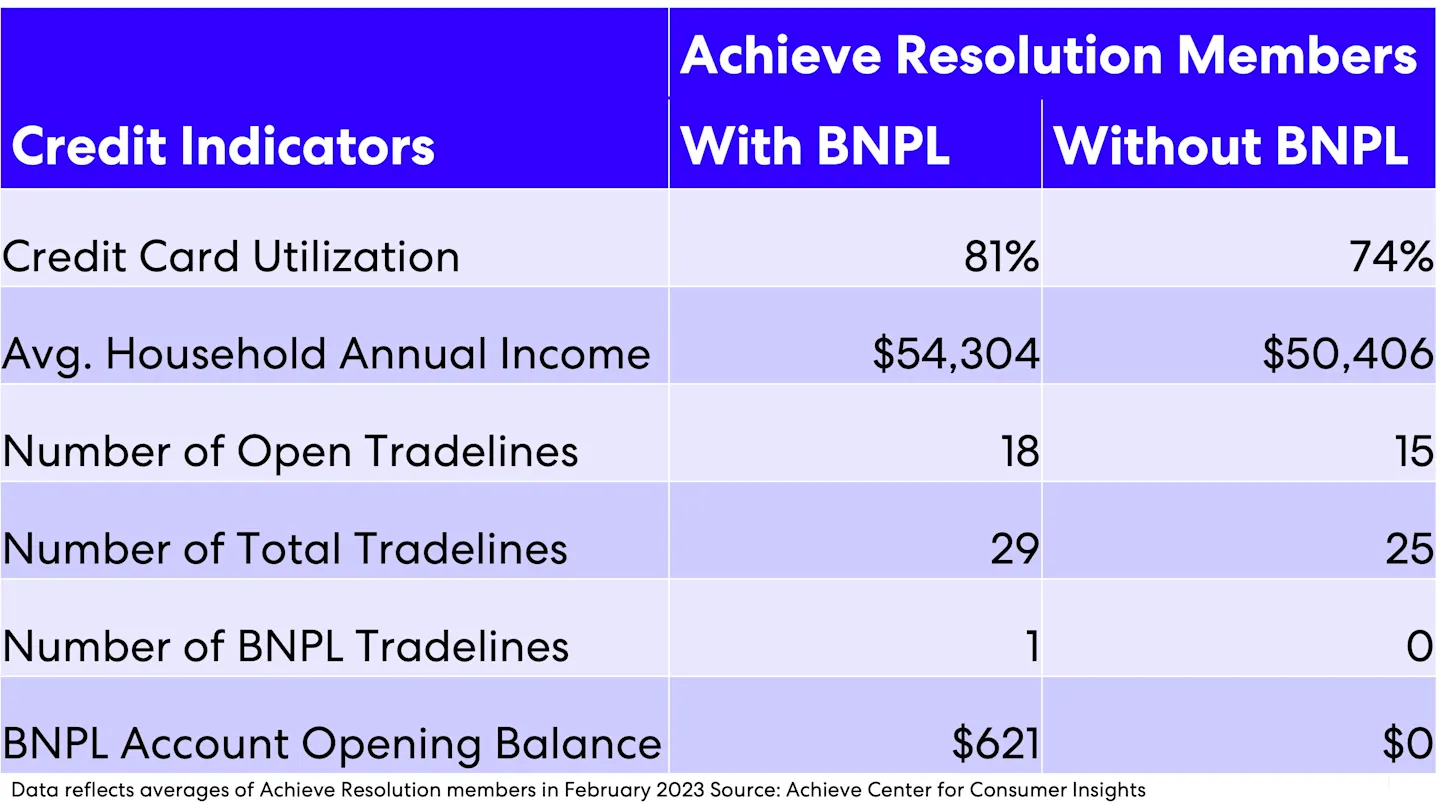

The CFPB’s findings echo many of our own observations about Achieve members enrolled in our debt relief program. As we’ve previously shared, Achieve Debt Relief members with BNPL loans on their credit reports have more open tradelines on their credit file and more total tradelines reported on their credit files. In other words, for many, BNPL isn’t an alternative to credit cards; it’s a way to stretch out the last remaining available credit on nearly maxed-out credit cards. Achieve members with BNPL accounts also had slightly higher credit card utilization rates than Achieve Debt Relief members without. They also had lower average credit scores than members without BNPL accounts. However, BNPL users had slightly higher household incomes.

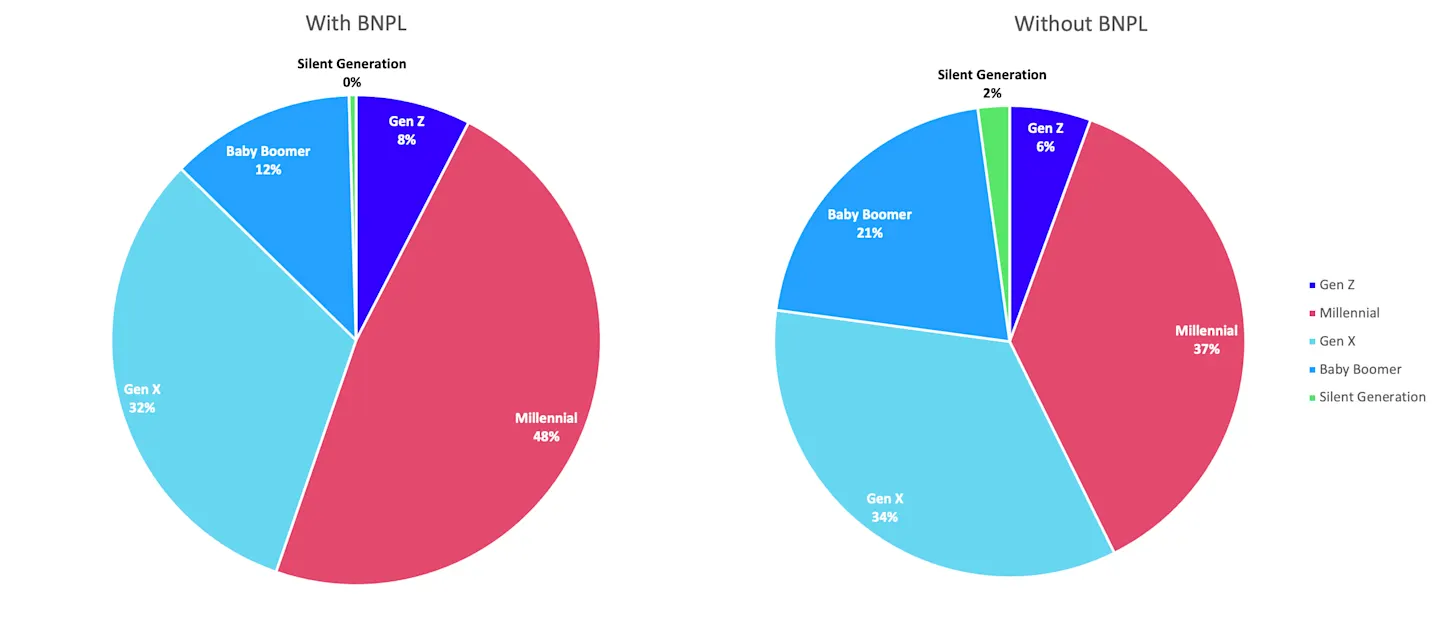

Young adults are a key demographic for BNPL providers, as many of these consumers have limited options for obtaining or building credit. The CARD Act, a 2009 law enacted in the wake of the Great Recession that’s designed to curb predatory credit card marketing and sales tactics, (particularly those targeting young adults). That’s delayed when many consumers begin applying for credit cards and other types of debt, but many types of BNPL loans (specifically those that don’t charge interest) aren’t covered by the law. And the CARD Act hasn’t stopped Americans in their 20s and 30s from becoming seriously delinquent on their credit cards at a faster pace than before the pandemic.

BNPL is not inherently evil or bad for consumers. Like all types of credit, BNPL can be an appropriate financial tool when used responsibly. But the nature of most BNPL lending is such that it’s difficult to keep track of transactions, both for consumers as well as other creditors that may have existing or future relationships with BNPL borrowers. And consumers who are accustomed to an ability-to-repay review as a condition of getting approved for credit risk being lulled into a false sense of security using BNPL.

It’s imperative for consumers to remain vigilant about their finances and protect themselves from getting over-extended when using BNPL or any other credit product. Given the rapid growth of BNPL and the potential downsides to consumers, it’s no wonder regulators around the globe are taking a closer look at BNPL providers to ensure adequate consumer protections are in place. One key difference between Apple Pay Later and some other BNPL offerings is that Apple intends to report users’ activity to the three credit bureaus, meaning these transactions may factor into borrowers’ credit scores. That’s great for consumers who don’t get overextended and may provide an opportunity for consumers with thin credit files to build a stronger credit profile, so long as they make timely payments. But borrowers who encounter trouble repaying their BNPL debts run the risk of hurting their long-term financial health.

Author Information

Written by

Analyst, Achieve Center for Consumer Insights

Related Articles

Americans in their 20s and 30s are becoming seriously delinquent on their credit cards at a faster pace than before the pandemic and approaching levels not seen since the Great Recession.

With financial volatility on the rise, it’s time to rethink how people use mobile apps to manage their money

Household debt is at record levels and all that borrowing is taking a toll on Americans’ mental and physical health.

Americans in their 20s and 30s are becoming seriously delinquent on their credit cards at a faster pace than before the pandemic and approaching levels not seen since the Great Recession.

With financial volatility on the rise, it’s time to rethink how people use mobile apps to manage their money

Household debt is at record levels and all that borrowing is taking a toll on Americans’ mental and physical health.