At Achieve, we're committed to providing you with the most accurate, relevant and helpful financial information. While some of our content may include references to products or services we offer, our editorial integrity ensures that our experts’ opinions aren’t influenced by compensation.

Debt Consolidation

How does a debt consolidation loan work?

Updated Jul 16, 2026

Written by

Reviewed by

Key takeaways:

Debt consolidation can be a smart financial move if you have multiple high-interest debts.

Usually, you consolidate debt by taking on a new loan and using it to pay off multiple smaller debts.

The debt consolidation loan should have better terms than the debts you consolidate, or it’s probably not worth taking.

See if you qualify. Apply Now

Committed. Smart. Savvy. These words describe someone who’s looking into a debt consolidation loan. Consolidating your debt shows that you’re ready to focus on lowering your debt and managing your finances more effectively. Researching your options shows that you have the patience and financial maturity to hold back until you know you’re making the right choice.

Any loan is a big decision, and that’s especially true when you’re already carrying debt. Once you understand how debt consolidation loans work, you can make a smart choice about the best path forward for you.

Debt consolidation loans work by simplifying your life

Debt consolidation means combining multiple debts. Most of the time, this involves taking on a new loan to pay off multiple smaller debts. Consolidating can make monthly bill paying easier because you have fewer debts to track. Debt consolidation may also deliver other benefits, like a lower payment or a better interest rate.

Debt consolidation loans

The most popular debt consolidation loans are home equity loans and personal loans. Also, some people consolidate debt with a balance transfer credit card—so we’ll explain that option as well.

Home equity loans

If you are a homeowner, you could consolidate debt with a home equity loan. A home equity loan is a second mortgage. To get a home equity loan, you need to be a homeowner with enough equity to borrow against. Equity is the difference between the home’s current market value and the amount you still owe on your mortgage. For example, if your home is worth $400,000 and you still owe $170,000 on your mortgage, you have $230,000 in equity.

All home equity loans are secured loans. You pledge the home as a guarantee that you’ll repay the loan. Because of this guarantee, lenders consider home equity debt consolidation to be fairly low-risk to them. That's why home equity loans have lower interest rates than most other kinds of financing.

The repayment term for a home equity loan is usually between five and 30 years. Longer terms can be helpful if your goal is to get the lowest possible payment.

Most home equity loan lenders charge a fee for making the loan (called an origination fee). Because this is a mortgage, your lender may require a property appraisal and title search. It’s possible to get a home equity loan in 10 to 14 days after you apply.

Home equity loans usually have a fixed interest rate, which means predictable payments for the life of the loan.

To get a home equity loan, you need sufficient equity, and you need to meet the lender’s requirements for credit score and income. At Achieve, a home equity loan might be a good way to consolidate debt with bad credit. If you let the lender use all or most of the loan funds to directly pay off other creditors, you can apply with a 640 credit score. Get started here to speak with a mortgage advisor.

Personal loans

You can also use a personal loan to consolidate high-interest credit card debt. Personal loans can be secured or unsecured, but most personal loans are unsecured. That means you don't have to borrow against something valuable that you own. There is no property to appraise, and that speeds things up a lot. If your income and credit meet the lender's guidelines, you could receive your money in as little as one to three days after you apply.

Personal loans usually have fixed interest rates and payments that don't change. This helps with budgeting. You can find personal loans in amounts ranging from $1,000 to $50,000 and even more, with repayment terms ranging from one year to over 10 years.

To get a personal loan, most lenders require a credit score of at least 620 to 680. You’ll also need to show proof of income. They’ll check your credit to review your other financial obligations so that they can be sure you can afford the payment on the loan you want. To talk to an Achieve loan consultant, start here.

Balance transfer credit cards

Balance transfers are not debt consolidation loans, but they are an option you might have heard of. Balance transfer credit cards offer an introductory period (usually six to 24 months) in which you pay little or no interest on transferred balances. If you’re approved, you can transfer your balances from other credit card accounts. There’s usually a 2-5% fee for each balance transfer.

Balance transfers can be risky. Some people transfer balances to a new card and then make new charges on the old cards. If that happens, you could end up with even more debt than you started with. It’s also tempting to transfer the balance again when the promotional interest rate expires. Moving balances back and forth between cards can quickly turn into a juggling act that’s very hard to keep up with. Eventually, the balls will drop. A balance transfer can give you an opportunity to make some serious headway against your debt, but it should be considered a one-time maneuver and part of a larger plan to get rid of your debt.

Compare debt consolidation loan options

Which type of debt consolidation loan should you get? The right choice depends on what you owe, whether you own a home, and the payment you can manage. Each option works a little differently.

Option | Collateral | Typical repayment term |

Personal loan | Usually none | 1 to 10+ years |

Home equity loan | Your home | 5 to 30 years |

Balance transfer card | None | Often 0% for 6 to 24 months |

A personal loan often funds the fastest and needs no collateral. Rates typically run higher than a home equity loan and lower than credit cards.

A home equity loan often has the lowest rate because your home is the collateral. Funding times are usually 10 days or longer.

A balance transfer card pauses interest during the 0% intro period. A transfer fee usually applies.

What credit score do you need to consolidate debt?

Lenders generally want a credit score in the mid-600s or higher, and a stronger score usually means a lower rate. Requirements vary by lender and by the type of loan.

For a personal loan, many lenders generally require a score of at least 620 to 680. For a home equity loan, you may be able to apply with a lower score. A balance transfer card usually calls for good credit.

The debt consolidation loan process

The debt consolidation process is fairly similar no matter which option you choose. First, you analyze your debt accounts and decide which ones you want to consolidate. Most people choose the debts with the highest interest rates.

Next, you'll decide what type of consolidation loan suits you best and compare loan rates and terms. In general, there's a trade-off between paying your loan off faster or getting a lower payment.

Once you've selected your loan, you'll apply online, in person, or by phone. Look for lenders that allow you to prequalify for a loan with a soft inquiry that doesn’t affect your credit score. If you're approved, you'll get a list of conditions you have to meet to finalize your loan. That might include submitting documentation like pay stubs and banking information.

Once the lender has everything it needs, it will finalize and fund your loan. In most cases, the lender transfers the money to your bank account. However, some lenders pay your creditors directly when you consolidate debt.

The inner workings of a debt consolidation loan

The right debt consolidation solution depends on the amount of your debt and on whether you’re looking to lower your payments or pay less total interest.

These three consumers—Daisy, Blake, and Fred—each have a different goal and amount of debt.

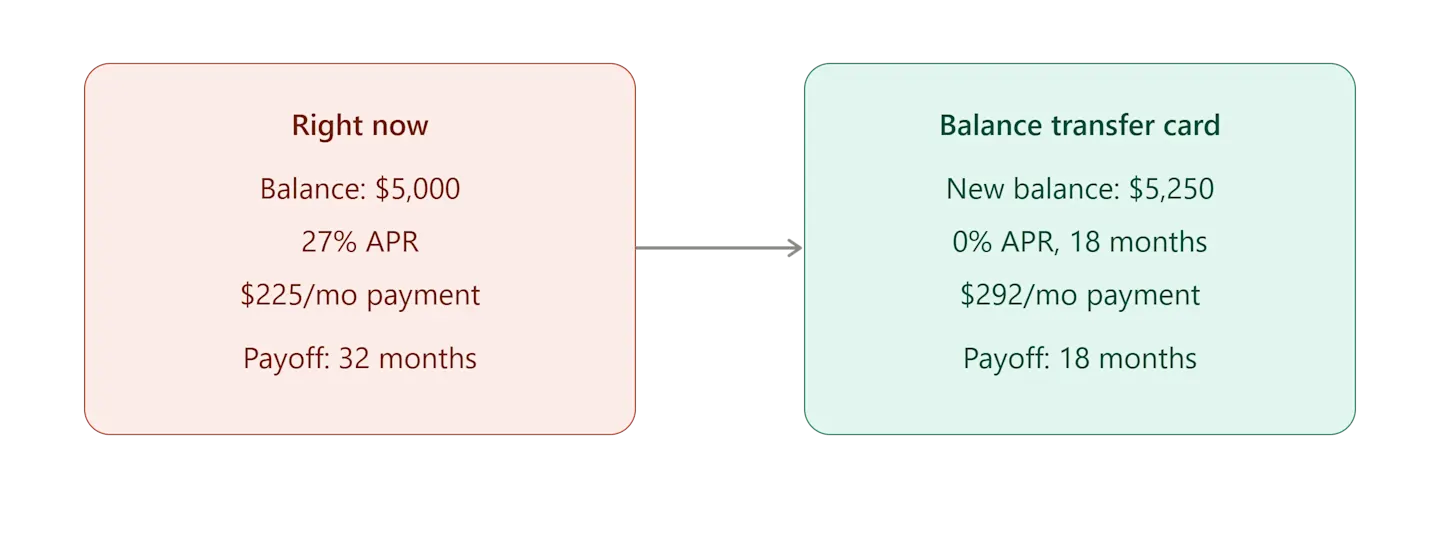

Daisy has $5,000 in credit card debt spread across four accounts at an average rate of 27%. She’s unhappy with the interest rate and the fact that her balance hardly drops after paying $225 a month. Time to pay off: 32 months.

Daisy chooses a balance transfer card with a 5% fee and 18 interest-free months. If she increases her payment and avoids adding any new charges to this card, she could clear her balance in a year and a half.

Daisy’s new payment is $292. Time to pay off: 18 months.

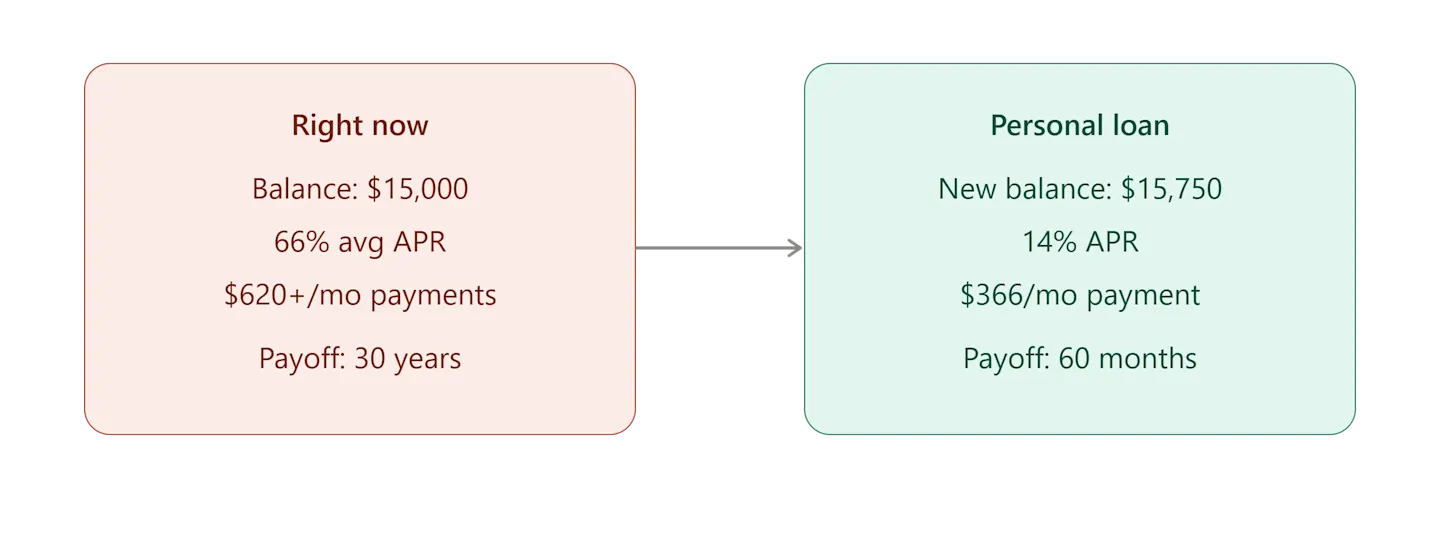

Blake has $13,000 in credit card debt at 30% interest. And he has rolled over a $2,000 auto title loan several times. Each title loan renewal costs $250. Title lenders don’t generally charge a straightforward interest rate. Instead, you’d pay high finance or rollover fees every two or four weeks. These charges equate to about 300% per year. That high rate means he’s paying an average of 66% APR on his $15,000 debt.

He’s paying about $620 a month now on the credit card balance. He’ll need 30 years to pay it off if he makes minimum payments. He pays as much as he can on the title loan but can’t figure out how he’ll pay it off within the next month before it renews again.

By consolidating his credit card debt and auto title loan into a personal loan, Blake can save on interest, escape his high-fee title loan, and get much-needed breathing room in his budget. Blake adds the lender fees to the loan and borrows a total of $15,750.

Blake’s new payment amount is $366. Time to pay off: 60 months.

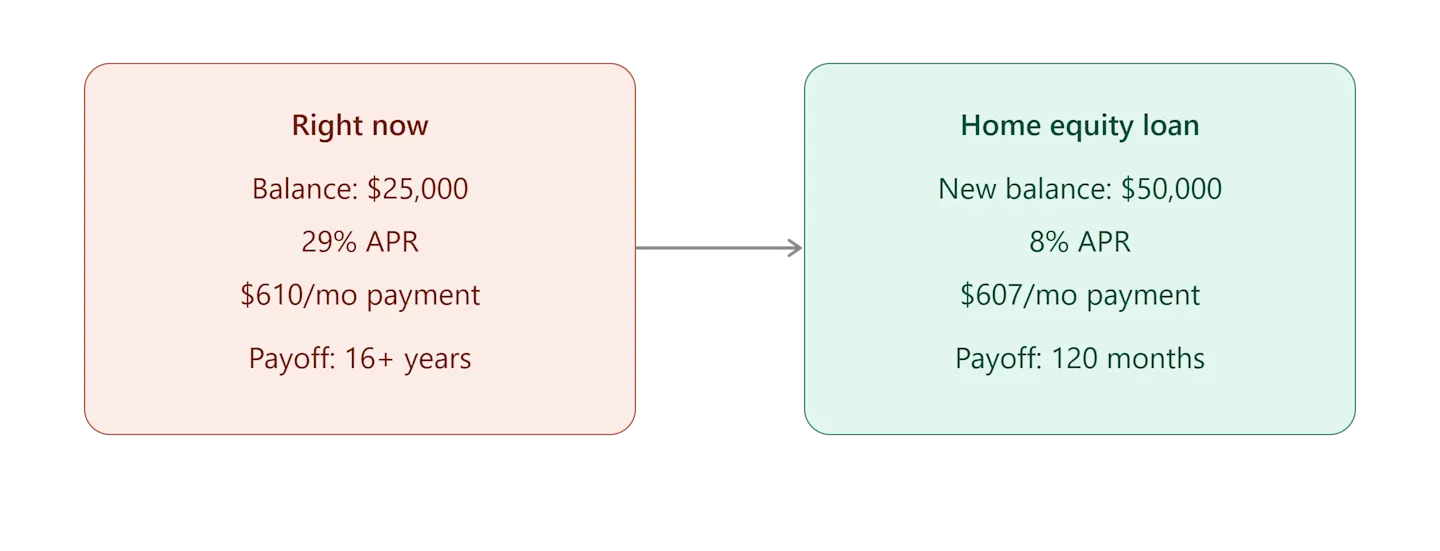

Fred owes $25,000 in credit card debt at an average rate of 29%, and he pays $610 per month but the balance hardly moves. At this rate, he’ll pay for more than 16 years. The bigger problem is that he also needs about $25,000 for dental work.

Fred opts for a $50,000 home equity loan to bring down the cost of his credit card debts and to cover the necessary healthcare expenses. His interest rate drops to 8%.

Fred’s new payment amount is $607. Time to pay off: 120 months.

To estimate your own numbers, try a debt payoff calculator.

Debt consolidation loan considerations

Debt consolidation isn't right for everyone or every situation. Here are some considerations that might mean a debt consolidation loan isn’t the best path forward.

Not everyone can qualify for a debt consolidation loan.

Only homeowners with sufficient equity can get a home equity loan.

A personal loan might not be big enough to meet your needs.

Debt consolidation doesn’t address spending problems. If you can't stop using your credit cards, adding a new loan to the mix could make things worse.

Don't consolidate if you can't get a real benefit. If the interest rate isn't better than your existing accounts, or the loan costs too much, look into other options.

Debt consolidation vs debt settlement

Debt consolidation and debt settlement are different. Debt consolidation uses a new loan to combine what you owe, and you repay the full amount over time. Debt settlement is a process where you, or a company you hire, ask your creditors to accept less than you owe but consider it payment in full.

Most people who choose settlement are already behind on their unsecured debt, since creditors generally negotiate only after an account is past due. Settlement may have a negative effect on your credit. Results are not guaranteed, and can vary.

| Debt consolidation | Debt settlement |

What it does | Combines debts into one new loan | Negotiates unsecured debt for less than you owe |

You repay | The full amount, over time | Less than the full balance, if creditors agree |

Credit impact | Small dip at first, may improve with on-time payments | Missed payments and settled accounts have a negative effect |

Best suited for | People with fair to excellent credit | People experiencing financial hardship |

Is debt consolidation right for you?

In most cases, debt consolidation makes sense when a new loan gives you a lower rate or a payment you can manage, and your spending is under control.

Consider it if:

You have steady income and fair to good credit.

You can afford to fully repay your debts

You qualify for a new loan that would lower the rate on your existing debt

You want to streamline your finances and reduce the number of payments you have to make each month

You have a plan to keep balances low after you consolidate.

Look at other options if:

Your credit needs work, since a higher rate could cost more than you save.

A loan large enough to cover your debt is hard to find.

Your income doesn’t cover all of your current expenses. A new loan doesn’t fix that on its own.

If a new loan isn’t realistic, a debt relief program may help you resolve unsecured debt for less than you owe.

If you can’t afford the payment on a new loan or debt consolidation isn’t in the cards for some other reason, you’re not completely stuck. Debt relief could reduce what you have to pay to get rid of your unsecured debt. Debt relief means negotiating with your creditors. You or someone working for you asks them to accept less than you owe and forgive the rest. You can get a free debt assessment and talk with an Achieve debt consultant who can help you determine if debt relief might be right for you.

Author Information

Written by

Gina Freeman has been covering personal finance topics for over 20 years. She loves helping consumers understand tough topics and make confident decisions. Her professional history includes mortgage lending, credit scoring, taxes, and bankruptcy. Gina has a BS in financial management from the University of Nevada.

Reviewed by

Kimberly is Achieve’s senior editor. She is a financial counselor accredited by the Association for Financial Counseling & Planning Education®, and a mortgage expert for The Motley Fool. She owns and manages a 350-writer content agency.

Frequently asked questions about how debt consolidation works

A debt consolidation loan can have positive and negative effects on your credit score. At first, your score will likely take a small hit. That's because applying for a new loan generates a credit inquiry. Each inquiry can have a small, temporary negative effect on your score. Also, the average age of your credit accounts is a factor that affects your score. Adding a new credit account lowers the average age of your accounts.

But paying off credit card debt lowers your credit utilization. Utilization is your credit card debt compared to your credit limits. If you have a $900 balance on a credit card with a $1,000 limit, your utilization is 90%. Lower utilization is better for your credit. Paying off credit card balances with a personal loan or home equity loan could have a positive impact on your credit.

Also, every on-time payment that you make on your new loan contributes to a healthy credit profile. Your payment history is the single most important factor that influences your credit score.

A home equity loan is a mortgage. Your house is the collateral (guarantee) for the loan. Home equity loans usually offer the lowest interest rates, but can cost more to set up and take longer to get. Home equity loans may offer the lowest payments because their terms can be as long as 30 years.

A personal loan usually doesn't require collateral. Personal loan interest rates run higher than home equity loans but almost always lower than credit cards. Personal loan terms range from 1 year to over 10 years.

Debt consolidation can help your finances if you are disciplined and careful. If you can get a lower interest rate, that frees up more money to pay off your debt faster. If your goal is a smaller payment, use it to get your finances under control. Put money away for an emergency fund. Take care of necessities you may have put off—like a car repair or medical procedure. Then commit to paying off the consolidation loan as fast as you can without borrowing any more.

Related Articles

Paying off multiple high-interest credit cards at the same time can be expensive and daunting. We show you how online debt consolidation can help.

Debt consolidation can help you pay off what you owe, but it isn't the only way to resolve the debt. Learn more here.

If you have high credit card debt, debt consolidation may be able to help you lower your monthly payments. Here’s how.

Paying off multiple high-interest credit cards at the same time can be expensive and daunting. We show you how online debt consolidation can help.

Debt consolidation can help you pay off what you owe, but it isn't the only way to resolve the debt. Learn more here.

If you have high credit card debt, debt consolidation may be able to help you lower your monthly payments. Here’s how.