At Achieve, we're committed to providing you with the most accurate, relevant and helpful financial information. While some of our content may include references to products or services we offer, our editorial integrity ensures that our experts’ opinions aren’t influenced by compensation.

Debt Basics

Debt stress

Sep 18, 2024

Written by

Reviewed by

Key takeaways:

Debt is a common part of life. Try not to beat yourself up for having some.

Recognizing debt stress is the first step to addressing it. You can’t deal with it until you acknowledge it and call it what it is.

It’s possible to lower your stress level long before you get rid of your debt.

Taking on debt can be a normal, even necessary, part of your everyday life.

People buy homes all the time and take out mortgages—they often can’t afford to do so without debt. Same with buying cars or getting a college education.

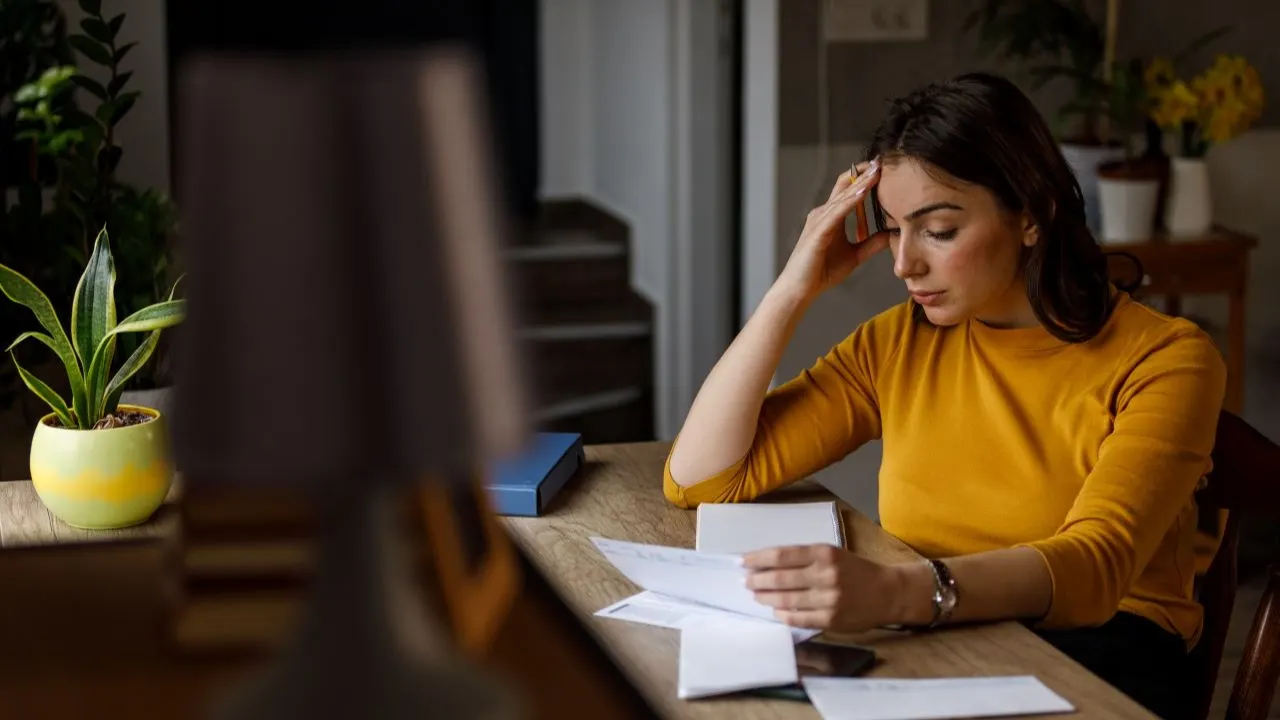

Sometimes, though, debt can get to the point where you end up feeling overwhelmed. If this is you, it’s possible you’re experiencing debt stress. Learning to spot it is the first step toward improving your financial situation— not to mention your overall well-being and your life.

What is debt stress?

Debt stress is a type of stress or anxiety that’s triggered by having debt. It isn’t necessarily just over the amount of debt you have. Rather, it’s about how you feel about your debt and how it’s affecting your day-to-day life. According to our June 2024 survey, 60% of consumers said the effects of debt and other personal financial issues have spilled over into other areas of their personal lives—from lost productivity at work to feelings of shame, exhaustion, and depression.

Say you feel like you have too much debt. You might owe quite a lot of money, and the bills feel neverending. You’re juggling multiple payments and aren’t sure whether there’s enough income to keep up or get ahead. You dread bill-paying time. You feel anxious, under an immense amount of pressure. You’re feeling debt stress.

Identifying debt stress: What are the signs?

Getting stressed over your debt can manifest in several ways. Here are some signs that you may be experiencing debt stress:

You feel scared to look at your bills. Feeling a regular sense of dread may be a sign you’re under debt stress. Some people dread the bills so much, they remain in denial about their situation until they get a wakeup call—like phone calls from creditors.

Anger comes easily. Experiencing anger can be a normal reaction to stress. For example, you might feel angry when your car breaks down, or when you find out a prescription will cost a lot more than you budgeted. When you’re angry, you may snap at your friends and loved ones for seemingly no real reason.

You feel tired when you make even little financial decisions. You’re probably busy juggling work, parenting duties, and other responsibilities like cleaning your home. And that’s on top of making sure you stay on budget and on top of your bills. If you find that any little decision—like where to find better grocery prices or which credit card to use when dining out—seems exhausting, you could be debt-stressed.

You believe you’re no good with money. It’s fine to make mistakes with money—it’s how we learn. But when you consistently feel like you’re incapable of getting any money decisions right, stress could be taking over.

It’s important to remember that whatever emotions or behaviors you have over your debt is normal—and according to our survey, many people have these feelings. Managing finances can take a lot of work, and there’s nothing wrong with how you’ve reacted. It’s also not useful to judge yourself too harshly for getting into whatever debt situation you’re in.

Instead, use these emotions or behaviors as a benchmark for seeing whether you’re feeling an unhealthy amount of stress over your debt.

Ways debt stress could affect your life

Debt stress can affect your mental and physical health, and spill over into other areas of life:

Relationships: Stress over debt may put a strain on your relationships. You may have disagreements over debts you share with your spouse. Maybe you feel you can’t share openly about your finances, feelings, or fears. According to a research report, couples are less likely to communicate openly about finances if they anticipate conflict.

Mental health: Feeling stressed about your debt could lead to mental health challenges, like depression and anxiety. If you’re already facing mental health challenges, financial stress could make it worse. Debt stress could lead you to feeling stuck, like you can’t get out of your current situation.

Physical health: Prolonged stress could lead to sleepless nights, which could affect your health. Stress could lower your immune response, or increase your risk for heart problems, stroke, digestive problems, and chronic pain flare-ups.

Practical tips for managing debt stress

Taking practical steps to tame your stress level is one of the best ways to care for yourself now and in the future. Ignore the urge to push it all away and ignore it.

Some best practices include:

Acknowledge you’re stressed and face your debt. Looking at the amount of money you owe feels hard. We get it. But ignoring what you owe could get you into more trouble. Instead, take your time and open each bill to look at the balance.

Create a budget. Knowing how to budget, to make plan for your money, could help you to understand where your money is going and whether you could use some of it to pay down your debt. You never know—you could be doing better than you think. Even if you’re behind on bills, figuring out how you could adjust your spending to put more toward debt is a great move. If budgeting feels overwhelming, use a simple money management app to make it easier.

Determine your debt priorities. Once you know exactly what your debts are and what each balance is, think about whether you could DIY your debt payoff. It may help to get a debt payoff buddy (lots of people in your life have debt they want to be rid of, too) or a financial coach.

Negotiate with creditors. You could try to negotiate your own debts. If you’re struggling financially, your creditors may be willing to work with you. They may offer a lower interest rate, a different payment plan, or even to accept less than the full amount you owe. They may also have a financial hardship program that allows you to skip one or more payments.

Take time to care for yourself: Stress can take a toll on you, so finding the time for true self-care is worth it. Find someone you trust who you can share your struggles with and look for activities that bring you joy. Even taking a walk and trying to go to bed earlier can make a world of difference.

What's next

Breathe. Give yourself a hug. You’re going to get to the other side of your debt. It may help to write a positive affirmation, such as “I’m capable of dealing with my debt,” and put it someplace visible.

Do the nuts-and-bolts work of assessing your situation. That means making a list of all your debts, the balances, the interest rates, and the status (whether you’re current or behind on payments). It’s hard to make a plan if you don’t know exactly what you’re dealing with. If you need a quick and easy way to see all your debts in one place and look your debt in the eye, try our free debt checkup.

Get your free credit reports from annualcreditreport.com and find a place to check your credit score for free (your bank or credit card online dashboard, or a free credit score website). This information will influence what options are available to you.

Take our Debt Fit™ quiz and get your personal Debt Fit Score™ to get a sense of your overall debt health. The score takes into account your debt situation, cash flow, financial habits, and goals and will give you personalized recommendations for what you can do to take better care of your debt.

Consider talking to Achieve’s debt experts or a financial coach to explore your options.

Author Information

Written by

Sarah is a contributing writer for Achieve. She is a financial counselor accredited by the Association for Financial Counseling & Planning Education®, and a writer for other Fortune 500 publications.

Reviewed by

Jill is a personal finance editor at Achieve. For more than 10 years, she has been writing and editing helpful content on everything that touches a person’s finances, from Medicare to retirement plan rollovers to creating a spending budget.

Frequently asked questions

Many people deal with overwhelming debt by creating a budget, acknowledging the stress, and sometimes seeking professional help.

This is something that gets easier with practice.

At first, talking about debt may feel awkward or embarrassing. Agree on some boundaries, like that you will be kind to each other and avoid negative comments. You might even set a 5-minute time limit at first, to lower the risk of letting the conversation escalate into something more emotionally charged.

Agree in advance on what the goal is for the conversation. Early conversations may just be for the purpose of gaining a comfort level with each other. Then you could move on to the goal of sharing all the details, no matter how squirmy they make you feel. The next goal could be to choose a path forward. Then your goal could be deciding together how to reach your goals.

Take your time. Offer frequent hugs if you’re the hugging type. Keeping at it is the best way to make money conversations flow more easily. Getting on the same page about money could help the two of you forge an even stronger bond as a couple.

Feeling stress is normal. Notice it and let yourself experience it. What you want to avoid is letting it get out of hand to the point where the stress is harmful to your overall well being. Visual reminders may help. Have a weekly debt checkup and congratulate yourself for every win, no matter how small. Focus your attention on the solution, and the actions you’re taking toward it. Connect with family and friends, and consider mentioning that you’re tackling your debt. Don’t be afraid to be loud and proud about managing to your budget. You might be surprised at how many people in your inner circle let you know that they are also dealing with debt or they have in the past. Shared experience is a great motivator because it really helps to know that you’re not alone, and you can get through this.

Related Articles

Debt stress can affect your physical and mental health. Learn what you can do now to stop it in its tracks.

Good debt helps you reach your goals at a cost that’s fair. Learn more about how to judge a debt for yourself.

You may be insolvent if you don’t have enough money to pay your debts. Insolvency could allow you to settle debt tax-free or wipe it out in bankruptcy.

Debt stress can affect your physical and mental health. Learn what you can do now to stop it in its tracks.

Good debt helps you reach your goals at a cost that’s fair. Learn more about how to judge a debt for yourself.

You may be insolvent if you don’t have enough money to pay your debts. Insolvency could allow you to settle debt tax-free or wipe it out in bankruptcy.